Financial reporting quality in enterprises in Vietnam

- University of Economics and Law, VNU-HCM

Abstract

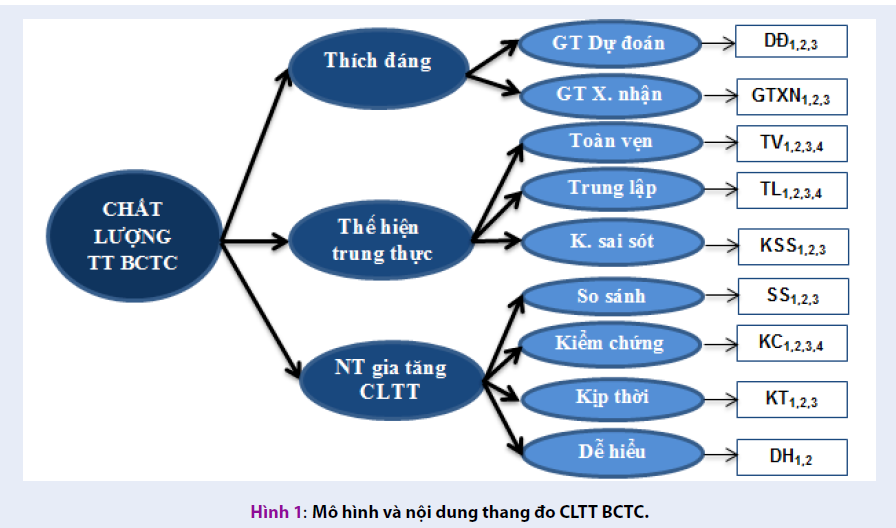

Financial reporting quality is one the most interesting topic, drawing many researchers and scientists' attentions in the field of a ccounting. Previous studies have shown that the measurement of financial reporting quality is developed in two main d irections: direct measurement (by operationalizing the qualitative characteristics) and indirect measurement (examines the level of earnings management; the specific elements in the annual report in depth,… as a proxy for financial reporting quality). This research aims to build, complete the measurement scale and assess the quality of financial reporting based on qualitative characteristics defined by FASB & IASB 2010. Qualitative research is used to build and complete the measurement scale of financial reporting through case studies using in-depth interviews and focus groups with respondents being specialists and experts in accounting field ( including. university lecturers, chief accountants, heads of internal control, Information technology managers and chief financial officers in enterprises in Vietnam). Quantitative research is used for measuring the financial reporting quality through survey on enterprises in Vietnam. The findings show that financial reporting quality is considered acceptable with average point being 3.7102/5. Among 3 qualitative characteristics of financial reporting quality, the enhancing characteristics are highly evaluated (4.2065/5) while the fundamental characteristics (relevance and faithful presentation) are considered as moderate (3.7032/5 and 3.5590/5).