Forecasting stock index based on hybrid artificial neural network models

- Banking University of Ho Chi Minh City, Viet Nam

- International University, VNUHCM, Viet Nam

- University of Economics and Law, VNUHCM, Viet Nam

Abstract

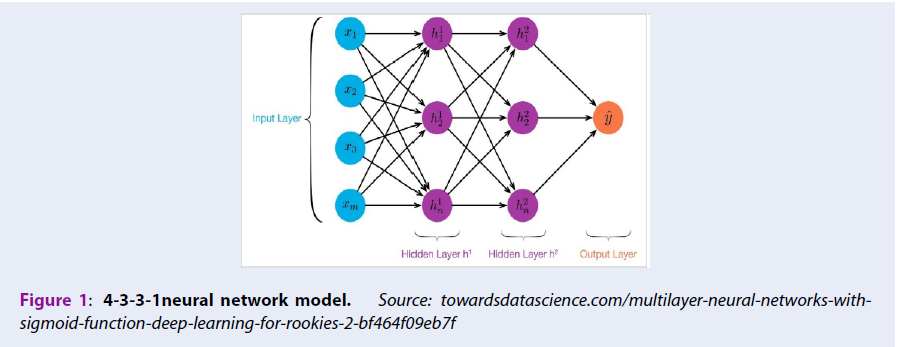

Forecasting stock index is a crucial financial problem which is recently received a lot of interests in the field of artificial intelligence. In this paper we are going to study some hybrid artificial neural network models. As main result, we show that hybrid models offer us effective tools to forecast stock index accurately. Within this study, we have analyzed the performance of classical models such as Autoregressive Integrated Moving Average (ARIMA), Artificial Neural Network (ANN) model and the Hybrid model, in connection with real data coming from Vietnam Index (VNINDEX). Based on some previous foreign data sets, for most of the complex time series, the novel hybrid models have a good performance comparing to individual models like ARIMA and ANN. Regarding Vietnamese stock market, our results also show that the Hybrid model gives much better forecasting accuracy compared with ARIMA and ANN models. Specifically, our results tell that the Hybrid combination model delivers smaller Root Mean Square Error (RMSE) and Mean Absolute Error (MAE) than ARIMA and ANN models. The fitting curves demonstrate that the Hybrid model produces closer trend so better describing the actual data. Via our study with Vietnam Index, it is confirmed that the characteristics of ARIMA model are more suitable for linear time series while ANN model is good to work with nonlinear time series. The Hybrid model takes into account both of these features, so it could be employed in case of more generalized time series. As the financial market is increasingly complex, the time series corresponding to stock indexes naturally consist of linear and non-linear components. Because of these characteristic, the Hybrid ARIMA model with ANN produces better prediction and estimation than other traditional models.