Consumer trust’s impact towards continuance usage intention regarding biometric authentication for digital payment of gen Z and the mediating role of perceived risk — Study in Ho Chi Minh City

- Canadian International School Vietnam, Ho Chi Minh City, Vietnam

- oane-Cardinal Schubert High School, Calgary, Canada

Abstract

This paper aims to evaluate the impact of consumer trust on continuance usage intention regarding biometric authentication for digital payment in Ho Chi Minh City, employing an alternative perspective that positions perceived risk as a mediator. Partial Least Squares Structural Equation Modeling was used to analyze data gathered from 313 undergraduate students in the city through personal contacts through a self-administered questionnaire distributed via Google Forms. The findings reinforce previously published results indicating that consumer trust significantly influences the intention to continue using biometric authentication in digital payments. Notably, consumer trust substantially impacts on perceived risk and encourages continued usage, contrasting with the prevailing findings in extant studies. The rise in trust correlates with a heightened interest in comprehending the associated dangers of biometrics. Gen Z raises a demand for risk disclosure, implicitly highlighting that payment providers must prioritize and implement promptly. This research contributes to the existing literature on e-commerce, particularly in the digital payment context, by proposing an interactional model demonstrating the relationship between consumer trust and continuance usage intention, with perceived risk serving as a mediating factor. This study underscores the importance of policymakers and businesses strengthening consumer trust within the digital payment landscape by developing and promoting stricter security regulations concerning biometrics in online transactions. Accordingly, performance risk, time risk and security risks emerge as critical components of perceived risk in evaluating the intention to continue using biometric authentication in digital payments. Therefore, service providers, technicians, and management must prioritize enhancing system performance to prevent disconnections, latency, or diminished responsiveness. Future research should aim to enlarge the sample size of diverse respondents or incorporate additional factors, such as perceived benefits and customer loyalty, thereby providing a more thorough understanding of biometric authentication in online payments.

Introduction

Digitalization has profoundly impacted the global financial landscape, initiating a transition from cash payments to online payment methods 1. The rapid development regarding technology, particularly in the areas involving information and communication, has led to the increasing prevalence of cashless payment systems, including mobile wallets and Internet banking1. In recent years, Vietnam has experienced significant economic transformation and digital revolution, with digital payment options becoming indispensable due to their convenience and efficiency1. These innovations have been seamlessly integrated into numerous Vietnamese daily lives, providing an easy and secure way to conduct transactions. The Coronavirus pandemic has further accelerated the adoption of online payment method1. In response to the aforementioned circumstances, the Vietnamese government, similar to various governments worldwide, has imposed strict social distancing and lockdown measures to mitigate the virus’s spread, thereby discouraging cash usage incredibly1. It has shifted towards digital payment methods as a safer alternative, enabling them to conduct transactions from the relatively safe homes during the pandemic. Vietnam’s adoption of cashless payment options has surged during the pandemic’s peak, with citizens increasingly relying on their digital banking platforms to navigate the economies within society. E-commerce’s success significantly depends upon consumers' continuance usage intention and confidence in secure online transactions. To further foster this trust and confidence, biometric solid authentication measures such as robust privacy and security protocols must therefore be enforced by e-commerce platforms.

Background Research

Digital Payment

Financial technology and e-commerce have revolutionized the global economy by enhancing customer experiences, simplifying transactions, and incorporating online payment systems into the public sector. Particularly in Vietnam, FinTech and e-commerce have seen exponential growth, driven by a tech-savvy population and increasing internet exposure, causing digital payments to be a vital component of the country’s economy. Digital payments have also become a crucial component of Vietnam’s expanding economic sector, driven by the rapid digitalization of financial services and evolving consumer habits or behaviors2. Platforms, particularly Shopee, hold the dominant market share with 63% of the Gross Merchandise Volume (GMV) and have significantly contributed to the transition toward online payment platforms. Shopee excels in seamlessly integrating payments within its system, facilitating a more convenient shopping and payment experience for users. As consumer confidence in online transactions increases, these platforms can capitalize on promotions and user-friendly interfaces, further solidifying their dominance in the Vietnamese e-commerce landscape 3. The rise in online shopping customers, particularly amongst the younger population, has led to a greater acceptance of cashless transactions. Shopee’s dominance in sectors such as home, beauty, fashion, and lifestyle highlights the impact of online payments on consumer spending, demonstrating these systems have integrated into Vietnam’s evolving retail market 3.

Biometric Authentication

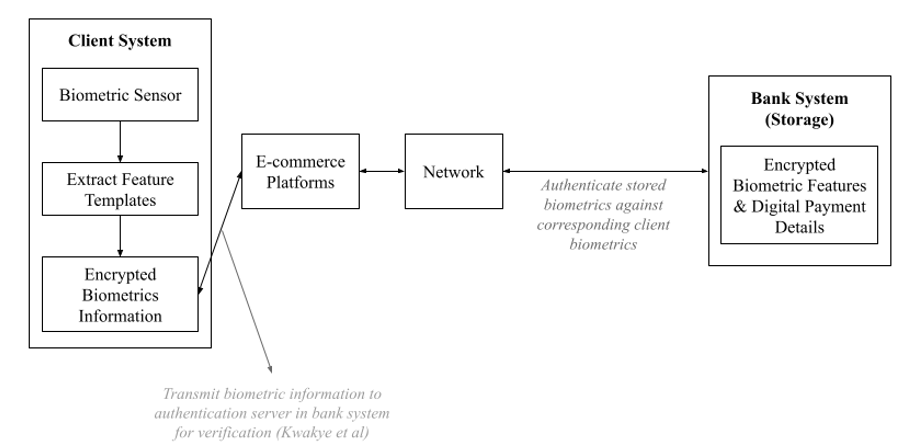

Biometric authentication in e-commerce transactions employs unique biological characteristics such as the eye’s iris 4, hand geometry, fingerprints, face, and voice recognition to verify a consumer’s identity 5. This process involves capturing user's above’ traits using a device’s webcam and extracting critical features through Principal Component Analysis (PCA), thereby identifying patterns within the image4. The extracted features would then be encrypted using the RSA algorithm and transmitted along with the user’s transaction details, to the bank system for verification/authentication. The encrypted biometrics data is compared with pre-stored information in the bank system’s database afterward to authenticate the user’s identity, enhance security, and mitigate fraud during transactions4. For users to proceed with the transaction, their biometrics information must undergo the verification process conducted by the bank system associated with the e-commerce platform, and this depends on whether the authentication step succeeds or fails4. The Figure 1 presented based on integrating previous studies 4, 6.

Modified Biometric Authentication Architecture Model

Biometric authentication has rapidly become a critical factor in Vietnam’s e-commerce landscape. This authentication method enhances security and builds customer trust, which are vital to the continuance usage intention (CUI) of online payment systems. Approximately 78% of Vietnamese consumers are recorded to prefer using biometric methods such as fingerprint and facial recognition compared to traditional PINs and passwords, citing these as more secure for identity verification during online transactions 7. The increase in e-commerce fraud and identity theft has prompted biometrics adoption in Vietnam, with over 38 million bank accounts and nearly 4 million e-wallets being linked to biometric authentication8. The widespread implementation of biometrics has significantly reduced fraud, as evidenced by a reported decrease in fraudulent bank accounts due to the Vietnamese government’s regulation for mandatory biometrics usage in high-value transactions7.

Through e-commerce platforms such as Shopee dominating the market, consumer trust (CT) has become a critical factor for the CUI regarding online payment methods. Biometric authentication plays a crucial role in reinforcing CT by ensuring that the users’ identities are secure during transactions. This is particularly significant in a rapidly expanding digital payment market dominating the e-commerce sector, with 50 companies providing such services in Vietnam 9. Consumers have higher probabilities toward the CUI of e-commerce platforms given that they possess confidence in financial data’s security, with biometrics serving as a reassurance through offering a distinctive and secure authentication method 10. Ultimately, biometric authentication in Vietnam enhances security, maintains customer trust (CT), and contributes to the continued growth of Vietnam’s e-commerce and FinTech sectors 8.

Literature Review

Theory of Trust

As proposed by Larue Tone Hosmer, the Theory of Trust is significantly crucial to understanding personal, organizational, and economic behaviors. Golembiewski and McConkie have asserted that no single variable has as profound an impact on interpersonal and group behavior as trust 11. Trust can be defined as an optimistic expectation concerning others’ actions and behaviors. This factor is particularly relevant under contexts characterized by dependence and vulnerability. Trust arises from implicit moral obligations that require individuals to safeguard other users’ interests, serving as a critical advocate for cooperation in economic and social interactions 11. Its significance in economic exchange is stated through Hirsch’s reemphasized that “trust was a ‘public good, necessary for the economic transactions’ success” 11. Opportunistic actions within a single market may generate short-term benefits. Nonetheless, these incur long-term costs in the form of diminished trust that can hinder “future acquisitions of cost-reducing and/or quality-enhancing assets”. Trust is thus, the probability that one economic consumer makes decisions and undertakes actions that are beneficial or, at a minimum, not detrimental to another11.

Moreover, Hill concluded that “reputation has an economic value”, highlighting its significant role in impacting others’ willingness to enter an exchange or transaction. This concept fundamentally arose from consistent trustworthy behavior, wherein trust in this circumstance is defined as the economically rational decision to commit to contractual obligations or promises11. Failure to adhere to such actions would ultimately lead to a reputation loss, “thereby diminishing future contracting opportunities” 11. Cummings further asserted that a higher level of trust diminishes the costs associated with monitoring performance and eliminates the necessity for control systems based on short-term financial outcomes11. Nevertheless, such systems could, as referenced by Hoskisson, have undesirable adverse impacts on reducing innovation and collaboration 11. It is significant to acknowledge that “trust did not replace the market or the hierarchy”, rather this factor complements and enhances authority, price, and economic transactions 11. Therefore, a critical aspect of trust’s definition is the expectation that the consequences of breaking trust would far exceed the benefits of maintaining it; otherwise, the decision to trust would merely reflect simple economic rationality 11.

Consumer Trust

Consumer trust (CT) is conceptualized as an exchange of belief between online payment providers and customers to satisfy consumers’ expectations12. In a cashless environment where digital payments have become increasingly prevalent, users’ intentions to adopt these platforms are highly driven by trust13, 14, 15. This fundamental aspect is ranked as the third most significant barrier to e-commerce success that drives consumer activities and engagement16, thereby “generating commitment that leads to strong, long-term” behavior17. A heightened technology fear due to a lack of CT may disrupt the relationship between CUI and actual usage regarding e-commerce platforms17. It is recorded that those having prior Internet usage experience oftentimes accumulate greater exposure to e-commerce, in turn fostering positive and favorable attitudes toward these platforms16. CT, being both a social and personal factor, is based on users’ anticipation regarding the deriving benefits in online payment usage, which can positively and directly impact continued usage intention (CUI) 17. CT is therefore essential for fostering and maintaining “a sustainable competitive advantage, increased revenue, and consumer satisfaction alongside loyalty”, thereby being a significant predictor regarding CUI in the e-commerce context 17.

Perceived Risk

Perceived Risk (PR), a multidimensional construct, is conceptualized as the probability negative outcomes might arise due to an economic event, thereby “impacting various entities such as individuals, businesses, organizations, or governments” 18. This factor has been a central focus in several empirical studies to deepen the understanding of consumer behaviors, particularly in the marketing field. Within the current digital payment context, PR plays a significant role in research concerning the acceptance of new technologies or innovations acceptance alongside shaping consumer behavior and trust. Consumers frequently associate digital payments with potential security vulnerabilities, including risks related to fraud, privacy breaches, and transaction errors19. These risk perceptions can significantly hinder users from engaging in online payment platforms20, and as a result, trust emerges as a vital mitigating factor given the context. PR can therefore be considered a function of uncertainty regarding a given behavior’s potential outcomes and their associated negative consequences21. It represents consumer uncertainty related to the loss or gain in a specific transaction.

Moreover, “the temporal separation between consumers and e-retailers”, challenges in anticipating contingencies and ambiguities in cybersecurity laws have contributed to an inherent uncertainty surrounding online transactions22. Therefore, secure and user-friendly digital payment platforms can therefore significantly reduce PR through implementing strong encryption, transaction guarantees, and effective security measures, fostering consumer confidence and trust in such context 23, 24. Empirical research has indicated that higher levels of CT correspond to lower PR, encouraging consumers to pursue and engage in online transactions frequently25. Within the digital payment context, PR plays a crucial role in influencing consumers’ decision-making, as users weigh the potential dangers against digital transactions' convenience. In circumstances where PR is high, customers would shift away from adopting and continuously using online payment platforms, despite their inherent benefits. Consequently, by effectively managing and minimizing PR through robust security measures, CT can be maintained and ensures the successful implementation of digital payment systems in this era.

Prior studies have asserted that PR is examined through multiple subdimensions 18, 26. This paper therefore examines the impact of six risk facets, including performance, financial, time, social, psychological, and security risks as mediators between CT and biometric authentication CUI. It is crucial to recognize that not every PR component mentioned previously influences the relationship between CT and biometric authentication CUI, as their impacts vary depending on the goods or services involved in online transactions.

Performance Risk

Performance Risk (PER) refers to the users’ perspectives regarding factors that can impact online payment platforms’ productivity and effectiveness 18. PER encompasses scenarios such as system malfunctions due to suboptimal internet speeds, server downtimes, and or maintenance periods alongside the failures in meeting consumers’ expectations regarding digital payments’ functionality and usability 18. Moreover, inconsistencies between advertisements by online payment providers and actual consumers’ usage experience further contribute to this risk18. Given that users are bound to encounter malfunctioning or flawed online payment methods, it is essential to mitigate PER. This thereby can enhance customers’ perceptions and facilitate CUI regarding online payment applications or systems18.

Financial Risk

Financial Risk (FR) is defined as the customers’ concerns regarding potential monetary losses experienced with online payment methods18. This risk may arise in situations such as errors in online payment transactions resulting in incorrect debits or financial losses not reimbursed by the payment provider. Moreover, for unclear reasons, users may experience a control loss over banking accounts. FR represents a significant type of PR as the potential consequences regarding money losses alongside the increase in banking malware attacks, can be severe18. This is particularly relevant for online payment applications directly linked to bank accounts, thereby being significantly riskier than traditional cash transactions.

Time Risk

Time Risk (TR) in online payment systems is a crucial factor impacting customer behavior and CUI, arising from concerns associated with time-related aspects, such as inconvenience or difficulties (Bland et al, 6). These concerns include the required time to proficiently use online payment applications and resolve issues such as transaction errors18. TR, including the learning process of adapting to new systems, transaction failure probabilities, and prolonged processing times can significantly lead to customer dissatisfaction, therefore “emphasizing the necessity for developers to enhance system usability and efficiency” 18.

Social Risk

Social Risk (SR) in online payment platforms can greatly impact consumers’ perspectives, attitudes, behavior, and CUI towards these applications18. These risks encompass the absence of support or approval from friends, family, and colleagues, and potential social status loss due to transaction errors and failures 18. Moreover, the reduced personal interactions inherent in online payment systems further exacerbate these risks Consumers perceive significant SR when digital payment methods are not accepted within their social frameworks and networks, resulting in a status or identity loss Developers should thereby focus on improving the social acceptance and perceived social benefits regarding their online payment systems to foster CUI and enhance customer satisfaction 18.

Psychological Risk

Psychological Risk (PYR) in online payment systems involves a perceived trust absence alongside feelings of unfamiliarity, unreliability, and fear18. These concerns stem from customers’ uncertainty regarding mobile payment platform usage, reflecting their mental apprehension, reluctance, and technological unreadiness to adopt such systems 18. To address these challenges along with enhancing consumer acceptance and CUI, digital payment developers and financial institutions should invest in education initiatives and user-friendly designs, prioritizing reliability and familiarity.

Security Risk

Security Risk (SER) is one of the most detrimental subdimensions of PR, involving the potential for external breaches that could result in the theft of money and baking account details during financial transactions. In the online payment context, security threats emerge through unauthorized access to bank accounts, resulting in fraud or hacking incidents27. Such risks can significantly impact the adoption of digital payment methods and consumers’ CUI. SR threatens users’ financial assets and depletes the trust these individuals possess in digital payment systems, leading to a reluctance to adopt online payment methods. It is therefore imperative to address SR through strong encryption and cybersecurity measures, which is crucial to upholding customer confidence and ensuring the CUI regarding digital payment applications.

Research hypothesis

Consumer Trust and Continuance Usage Intention

The relationship between consumer trust (CT) and CUI regarding online payment systems is essential for comprehending the long-term adoption of these payment methods. Trust is conceptualized as the belief that an online payment method would provide its users reliability and security, thereby directly impacting a user’s intention to continue using the service28. Consumers who perceive online payment platforms as secure are more inclined to overlook the associated risks, such as fraud or data breaches, thus fostering a sense that encourages CUI. When trust is at a high point, consumers exhibit confidence in the security regarding transactions and their personal data, increasing the probability of repeated engagement with the payment platform28. Conversely, in the absence of trust, users are prone to abandon online payment services after initial usage, as perceived risks outweigh perceived benefits. Consequently, it is essential to establish and sustain trust in online payment providers to ensure long-term usage and foster consumer loyalty. Therefore, the first hypothesis is proposed:

H1: Consumer Trust (CT) positively influences Continuance Usage Intention (CUI).

Consumer Trust and Perceived Risk

Consumer trust (CT) and perceived risk (PR) relationships are similarly significant in shaping consumer behavior and decision-making processes within an online payment environment. Given this context, CT is defined as consumers’ perceptions that digital payment platforms would manage economic transactions by anticipated expectations, thereby CT has been examined as a crucial factor in mitigating PR28. These applications depend upon mobile networks and systems that can be perceived as vulnerable and thus, the risks associated with online payments are much greater compared to traditional alternatives such as cash and coins. The Theory of Trust mentioned in the previous section highlights that users are more inclined to increase their trust in products and services when perceiving lower associated risks or a complete absence of risk 11.

The relationship between CT and PR is due to the inherently uncertain and doubt, driven by technologies’ presence within digital payment contexts 29. Kim et al characterized PR as the consumers’ uncertainty regarding their decisions’ outcomes, and therefore is identified as “an important barrier for consumers considering making an online purchase”29. It is argued that a lack of trust has been identified as a primary reason consumers refrain from engaging in online payment and transactions29, thereby demonstrating CT and PR significance in impacting purchasing decisions. Empirical studies have consistently demonstrated a negative correlation between CT and PR, indicating that enhancing CT leads to lower PR. The research on cashless systems indicates that PR has a negative impact on consumers’ intentions to adopt and use digital payments 30.

Nonetheless, recent studies have provided contrasting unexpected evidence, indicating that “CT has a statistically significant and positive impact on PR”31. Goyal et al., Ling et al., Kassim NM and Ramayah have established certain risk dimensions that positively impact trust, thereby highlighting the positive correlation between CT and PR. Goyal et al have further referenced the cognitive dissonance theory, positing that as individuals increase trust or “justify the legitimacy of an authority to cope with their dependence on it, they should be motivated to avoid information that could potentially rupture this trust”31. Nevertheless, given the various empirical studies and evidence regarding the relationship between CT and PR, the hypothesis below is put forth:

H2: Consumer Trust (CT) negatively influences Perceived Risk (PR).

Perceived Risk and Continuance Usage Intention

PR within the context of technology-based services refers to “the potential for loss in the pursuit of a desired outcome from using the service” 32. Previous research has indicated that as consumers assess a technology-based platform, beliefs regarding the service and its potential usage are formulated, which may encompass risk-related perceptions. These significantly influence users’ assessment of usage risks associated with online payment applications, thereby impacting their intentions toward CUI 32. Adopting digital payment platforms inherently involves risks, including unforeseen negative outcomes or financial losses for. Such that, individuals exhibit greater risk aversion than risk-seeking behavior, PR is an essential variable in anticipating and determining prospective behavior of online payment users 32. Having that said, numerous studies have indicated that PR directly and negatively impacts CUI, highlighting the fact that consumers’ willingness to adopt and use digital payment applications diminishes as their risk perception increases.

Similar to the relationship with CT, an argument exists that PR positively impacts CUI. 33 certain studies have reported that the relationship between PR and CUI is either insignificant or even positively correlated31. Further results suggest that users neglect potential risks due to their perception regarding the possibility that such events would not occur, alongside the “confidence in service providers and governmental support” 31. Consumers therefore are more concerned regarding trust, and oftentimes disregard risks, given that there is reliability towards online payment providers31. Nevertheless, in alignment with common findings regarding the relationship between PR and CUI, the hypothesis is proposed as below:

H3: Perceived Risk (PR) negatively influences Continuance Usage Intention (CUI).

Nonetheless, there is an ongoing argument regarding PR’s role alongside its relationship with CT and CUI. Compared to studies prior to the year 2020, recent research has evoked that CT positively influences PR and, in turn, has a favorable impact on CUI. Therefore further investigation is essential to elucidate the significance and importance of PR among Gen Z residing in Ho Chi Minh City. Thus, another hypothesis is suggested:

H4: The relationship between Consumer Trust (CT) and Continuance Usage Intention (CUI) is mediated by perceived risk (PR).

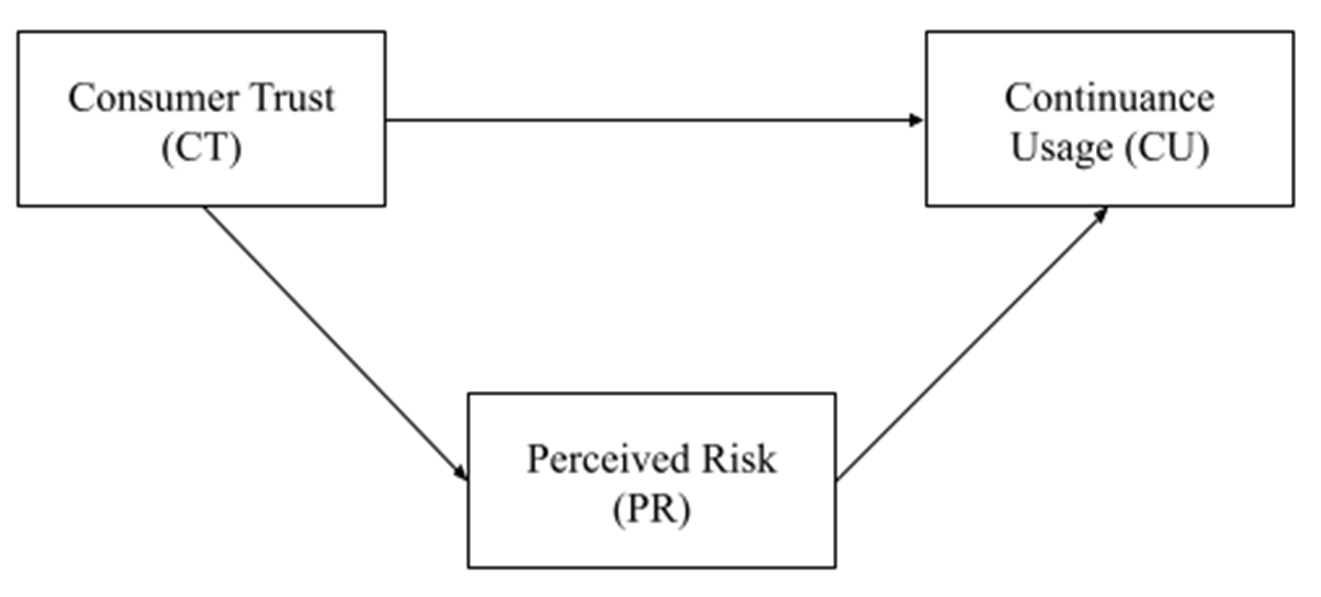

Consistent with the previously presented arguments and explanations, the conceptual framework is provided in the Figure 2.

Proposed Research Model

Methodology

Respondent

The target respondents for this study are Gen Z individuals born between 1997 and 2006, residing or studying in Ho Chi Minh City, and currently using digital payment methods alongside authenticating transactions via biometrics. These targeted participants must have a monthly income higher than 5 million VNĐ. With biometric authentication being mandatory in Vietnam’s current context for transactions exceeding 10 million VNĐ, individuals with a monthly income above this threshold have a higher probability of possessing greater opportunities for savings or adequate account balances to facilitate payments that necessitate biometric verification. To diversify the survey’s population, respondents’ majors are classified into distinct categories, including sciences, technology, social sciences and humanities, economics and business administration, law, medicine, and pharmacy, among others.

Instrument Development

The questionnaire content has been translated into Vietnamese to accommodate the targeted participants, with them being native speakers of this language. Before the survey’s formal distribution, a pilot test was conducted with 50 individuals to ensure respondents comprehended the questionnaire substance smoothly and effectively. Afterward, Google Forms is employed as a web-based platform for questionnaire distribution and data collection platform. The Likert scale, ranging from “strongly disagree” to “strongly agree” is employed to measure the question items based on the theoretical framework 34. The survey will be prolonged within a month starting in late July 2024.

Measurement Scales

This study adopted the scale derived from prior research to evaluate the constructs and their respective components. As mentioned previously, PR is a multidimensional concept evaluated through six components, including PER, FR, TR, SR, PYR, and SER. Since this study primarily focuses on digital payment, the adopted measuring scale must align with the research objective. Our study incorporates updated measurement scales specific to digital-oriented systems alongside the original measurement scale,. Referring to PR’s measurement scale, Featherman and Pavlou in the initial successfully developed subconstructs to assess PR, that is measuring PER, FR, TR, and PYR. Rooted in this origin, several academicians have expanded and refined the measurement scale for PR over the past two decades, resulting in six major components, referred to as PER, FR, TR, SR, PYR, and SER. Consequently, including revised measurement scales is essential for this research. CT and CUI are considered as unidimensional variables, each with specific items for measurement. Table 1 presents factors and sources adopted for this paper’s measurement scale.

Constructs’ Sources

|

Construct |

Source |

|

Performance Risk (PER) |

Featherman and Pavlou (2003); Roy et al. (2017); Chen (2013) |

|

Financial Risk (FR) |

Featherman and Pavlou (2003); AlSomali et al. (2009); Chen (2013) |

|

Time Risk (TR) |

Featherman and Pavlou (2003); AlSomali et al. (2009) |

|

Social Risk (SR) |

Venkatesh et al. (2012); Putri (2018); Featherman and Pavlou (2003); AlSomali et al. (2009) |

|

Psychological Risk (PYR) |

Featherman and Pavlou (2003); Martins et al. (2014); Chen (2013) |

|

Security Risk (SER) |

Aldas-Manzano et al. (2009); AlSomali et al. (2009) |

|

Consumer Trust (CT) |

Gefen (2000); Zmijewska (2004); Putri (2018) |

|

Continuance Usage Intention (CUI) |

Venkatesh et al. (2012); Thong & Xu (2012) |

Results and Discussion

This paper employs Smart PLS 3.2.9 for conducting Partial Least Squares Structural Equation Modeling (PLS-SEM)35. The evaluation process requires first executing the measurement model and afterward, the structural model. The former model assesses each construct’s reliability and validity whilst the latter is responsible for hypothesis testing.

The demographic results are provided in Table 2. Upon completing the survey, a total of 313 valid questionnaires (n = 313) have been gathered for data analysis. The gender distribution demonstrates that 50.8% of respondents are female, whilst 49.2% are male; with participants primarily pursuing Economics, Business, and Management, accounting for 38.34%. Their monthly income ranges from 5 to 10 million VNĐ and those earning more than 18 million VNĐ per month only comprise less than 10%. Nonetheless, this distribution is rational as the surveyed respondents are Gen Z and are currently pursuing their bachelor’s degree studies, limiting opportunities for acquiring a well-paid part-time position.

Respondents Demographics

|

Characteristics |

Items |

Number |

Percentage (%) |

|

Gender |

Female |

159 |

50.8 |

|

Male |

154 |

49.2 | |

|

Major |

Economics, Business, and Management |

120 |

38.34 |

|

Engineering and Technology |

84 |

26.84 | |

|

Law |

17 |

5.43 | |

|

Medical Health and Pharmacy |

27 |

8.63 | |

|

Natural Science |

10 |

3.19 | |

|

Social Sciences and Humanities |

10 |

3.19 | |

|

Other |

45 |

14.38 | |

|

Monthly Income |

> 5-10 million |

255 |

81.47 |

|

> 10-18 million |

38 |

12.14 | |

|

> 18-32 million |

7 |

2.24 | |

|

> 32 million |

13 |

4.15 |

Measurement Model

Perceived risk assessment as a second-order construct

Given that PR is a second-order construct, this paper employs a two-stage approach to analyze the proposed model. In the first stage, an analysis regarding the six components of the construct is conducted to determine its index. The relationship among CT, PR, and CUI is subsequently examined collectively. An appropriate assessment should be employed since PER, FR, TR, SR, PYR, and SER are reflective measurement scales. Therefore, it is essential to evaluate these subconstructs’ reliability and validity.

To begin with, reliability is evaluated at both the indicator and construct levels. For indicator reliability, the outer loadings value must be above 0.7 36, where the constructs’ reliability is reflected through Cronbach’s Alpha and Composite Reliability (CR). DeVellis and Thorpe has stated that a construct is considered reliable when its Cronbach’s Alpha is no less than 0.7. Furthermore, Chin designates a threshold of 0.6 for CR in exploratory research, whilst this requirement is higher, at least 0.7 regarding explanatory research. Due to adopting prior measurement scales with few modifications to be suitable for the research context, this paper is recognized as explanatory research with CR value starting at 0.7. Table 3 and Table 4 present results from the reliability assessment, encompassing outer loadings, Cronbach’s Alpha, and CR. Notably, PFR1, SR2, and SR3 do not meet reliable criteria, leading to the fact that these items being discarded; however, FR with a Cronbach’s Alpha of 0.69 remains acceptable as it is extremely close to the threshold of 0.7.

Outer Loadings

|

PER |

FR |

TR |

SR |

PYR |

SER | |

|

PER2 |

0.75 | |||||

|

PER3 |

0.84 | |||||

|

PER4 |

0.77 | |||||

|

FR1 |

0.81 | |||||

|

FR2 |

0.78 | |||||

|

FR3 |

0.77 | |||||

|

TR1 |

0.78 | |||||

|

TR2 |

0.80 | |||||

|

TR3 |

0.82 | |||||

|

TR4 |

0.82 | |||||

|

SR1 |

1.00 | |||||

|

PYR1 |

0.87 | |||||

|

PYR2 |

0.77 | |||||

|

PYR3 |

0.87 | |||||

|

PYR4 |

0.77 | |||||

|

SER1 |

0.80 | |||||

|

SER2 |

0.83 | |||||

|

SER3 |

0.78 | |||||

|

SER4 |

0.72 |

Outer Loadings

|

Cronbach’s Alpha |

Composite Reliability (CR) | |

|

PER |

0.70 |

0.83 |

|

FR |

0.69 |

0.83 |

|

TR |

0.82 |

0.88 |

|

SR |

1.00 |

1.00 |

|

PYR |

0.84 |

0.89 |

|

SER |

0.79 |

0.86 |

Furthermore, convergent validity and discriminant validity are examined for the validity assessment. The Average variance extracted (AVE) quantifies the variance captured by a construct about measurement error and must be above 0.5 to ensure that the latent construct accounts for more than half of the variance in its indicators 37. The Heterotrait-Monotrait ratio of correlations (HTMT) between pairs of factors should remain below 0.90 38 and the HTMT results derived from the bootstrapping test must not exceed 1.00. Table 5, Table 6, Table 7 present the outcomes for AVE and HTMT, with values that satisfy the established assessment criteria.

AVE

|

Average Variance Extracted (AVE) | |

|

PER |

0.62 |

|

FR |

0.62 |

|

TR |

0.65 |

|

SR |

1.00 |

|

PYR |

0.67 |

|

SER |

0.61 |

Heterotrait-Monotrait Ratio (HTMT)

|

FR |

PER |

PYR |

SER |

SR |

TR | |

|

FR | ||||||

|

PER |

0.63 | |||||

|

PYR |

0.62 |

0.59 | ||||

|

SER |

0.78 |

0.68 |

0.52 | |||

|

SR |

0.54 |

0.55 |

0.59 |

0.45 | ||

|

TR |

0.61 |

0.72 |

0.67 |

0.53 |

0.61 |

HTMT Bootstrapping

|

Original Sample (O) |

Sample Mean (M) |

2.5% |

97.5% | |

|

TR → FR |

0.61 |

0.61 |

0.47 |

0.75 |

|

TR → PER |

0.72 |

0.72 |

0.60 |

0.82 |

|

TR → PYR |

0.67 |

0.67 |

0.55 |

0.78 |

|

TR → SER |

0.53 |

0.53 |

0.40 |

0.66 |

|

TR → SR |

0.61 |

0.60 |

0.50 |

0.70 |

|

SR → FR |

0.54 |

0.54 |

0.41 |

0.65 |

|

SR → PER |

0.55 |

0.55 |

0.43 |

0.66 |

|

SR → PYR |

0.59 |

0.59 |

0.49 |

0.69 |

|

SR → SER |

0.45 |

0.45 |

0.33 |

0.57 |

|

PYR → FR |

0.62 |

0.62 |

0.49 |

0.76 |

|

PYR → PER |

0.59 |

0.59 |

0.46 |

0.71 |

|

SER → FR |

0.78 |

0.78 |

0.64 |

0.90 |

|

SER → PER |

0.68 |

0.68 |

0.55 |

0.80 |

|

SER → PYR |

0.52 |

0.52 |

0.38 |

0.65 |

Consumer trust, perceived risk & continuance usage intention assessment as a first-order construct

Following the initial stage that established indices for PR’s six components, the second stage focuses on evaluating the measurement model among 3 constructs: CT, PR, and CUI. PR and CT are considered formative models, whereas CUI is a reflective model; therefore, appropriate suitable evaluation criteria should be rigorously implemented.

Indicator collinearity and indicator reliability are two essential criteria that a formative model has to surpass. The outer Variance Inflation Factor (VIF) when less than 3.0 provides sufficient evidence to conclude that collinearity is not present among the constructs39, 40. Subsequently, bootstrapping is necessary to analyze the outer weights, where items with a p-value lower than 0.05 are considered statistically significant41. Smart PLS Report indicates that every outer VIF’s values exceed the threshold, with results in Table 8. Nonetheless, the p-value for the direction from FR, PYR, and SR to PR is significantly greater than 0.5, thus these three components must be eliminated.

Outer VIF

|

VIF | |

|

CT3 |

1.69 |

|

CT4 |

1.77 |

|

CT5 |

1.78 |

|

PER |

1.64 |

|

SER |

1.41 |

|

TR |

1.50 |

Conversely, in Table 9, the p-value reflecting PER influences on PR does not meet the criteria, with its p-value being 0.06, and in such circumstances, the outer loadings should be further taken into account. Table 10 demonstrates PER’s outer loading value to be 0.82, which exceeds 0.5, and therefore, PER remains significant 41. Based on the results for indicator collinearity and indicator reliability, the two formative models, CT and PR are considered reliable and no collinearity exists among the remaining indicators.

Outer Weights

|

Original Sample (O) |

Sample Mean (M) |

Standard Deviation (STDEV) |

T Statistics (|O/STDEV|) |

P Values | |

|

CT3 → CT |

0.49 |

0.49 |

0.08 |

6.41 |

0.00 |

|

CT4 → CT |

0.31 |

0.31 |

0.09 |

3.40 |

0.00 |

|

CT5 → CT |

0.37 |

0.37 |

0.08 |

4.44 |

0.00 |

|

PER → PR |

0.36 |

0.36 |

0.19 |

1.87 |

0.06 |

|

SER → PR |

0.34 |

0.33 |

0.17 |

2.02 |

0.00 |

|

TR → PR |

0.52 |

0.51 |

0.17 |

3.13 |

0.00 |

Outer Loadings

|

CT |

CUI | |

|

CT3 |

0.88 | |

|

CT4 |

0.81 | |

|

CT5 |

0.84 | |

|

PER |

0.82 | |

|

SER |

0.75 | |

|

TR |

0.86 |

Being a reflective model, the CUI assessment is conducted similarly to the first stage mentioned previously. Table 11, Table 12 indicate that every item in CUI’s construct satisfies reliability and validity requirements.

Outer Loadings

|

CUI | |

|

CUI1 |

0.84 |

|

CUI2 |

0.86 |

|

CUI3 |

0.85 |

|

CUI4 |

0.81 |

Cronbach’s Alpha, CR, and AVE

|

Cronbach’s Alpha |

Composite Reliability (CR) |

Average Variance Extracted (AVE) | |

|

CUI |

0.86 |

0.91 |

0.71 |

Structural Model

Alongside the measurement model, it is crucial to evaluate the structural model, with inner VIF is used for identifying the collinearity’s existence. Subsequently, the statistical significance and relevance of the path coefficients are assessed through bootstrapping for hypothesis testing purposes. The power for independent variables in explaining dependent variables is quantified R-squared values. Furthermore, the effect size is examined through the f-square outcomes with the aim of clarifying the importance of the independent variable over the dependent variables.

The Inner VIF when less than 3.0 indicates the absence of collinearity 39, 40. Table 13 demonstrates that the Inner VIF values are lower than 3.0, confirming that collinearity does not exist between independent variables (CT and PR) and dependent variables (PR and CUI).

Inner VIF

|

CT |

CUI |

PR | |

|

CT |

1.16 |

1.00 | |

|

CUI | |||

|

PR |

1.16 |

Based on the path coefficients in Table 14, both CT and PR significantly influence CUI, as evidenced by p-values below 0.05 36. Notably, CT generates a higher influence on CUI than PR, with both variables resulting in a positive direction towards CUI. The PR’s indirect specific effects as a mediator require further evaluation.

Path Coefficients

|

Original Sample (O) |

Sample Mean (M) |

Standard Deviation (STDEV) |

T Statistics (|O/STDEV|) |

P Values | |

|

CT → CUI |

0.65 |

0.65 |

0.04 |

15.78 |

0.00 |

|

CT → PR |

0.37 |

0.38 |

0.05 |

7.01 |

0.00 |

|

PR → CUI |

0.13 |

0.13 |

0.05 |

2.73 |

0.01 |

Table 15 provides evidence to conclude that PR mediates the relationship between CT and CUI, with a p-value of 0.01 and an original sample value of 0.05, indicating that PR delivers an indirect effect from CT to CUI. Regarding explanatory power, CT and PR can explain 50% of CUI, whilst their explanatory capacity in the relationship between CT and PR is weaker (R = 0.14) — results are included in Table 16. According to Cohen’s criteria, CT has a more significant impact on CUI, as its f-square approach is 0.73. Conversely, the impact sizes of CT on PR and PR on CUI are negligible, as their f-square values are below 0.2 (Table 17).

Specific Indirect Effects

|

Original Sample (O) |

Sample Mean (M) |

Standard Deviation (STDEV) |

T Statistics (|O/STDEV|) |

P Values | |

|

CT → PR → CUI |

0.05 |

0.05 |

0.02 |

2.44 |

0.01 |

R-square

|

R2 |

R2 Adjusted | |

|

CT |

0.50 |

0.50 |

|

CUI |

0.14 |

0.14 |

f-square

|

CT |

CUI |

PR | |

|

CT |

0.73 |

0.16 | |

|

CUI | |||

|

PR |

0.03 |

Implicitly, CT maintains a significant position in determining CUI, exerting the strongest impact. Consequently, any changes related to CUI in biometric authentication for digital payments should be considered from CT’s aspect. Remarkably, despite the weak influence compared with CT, PR with its components — PER, TR, and SER positively contribute to enhancing CUI. As demonstrated in Figure 3and Table 18, H1 and H4 are supported whereas the results for H2 and H3 are reversely supported. To be more specific, CT positively impacts CUI (β = 0.65, t = 15.78, p-value < 0.05), where this relationship is mediated by PR (β. =0.05, t = 2.44, p-value < 0.05). In contrast, both CT (β = 0.37, t = 7.01, p-value < 0.05) and PR (β = 0.13, t = 2.73, p-value < 0.05) indicate positive impacts on PR and CUI respectively, contrary to the negative direction proposed the hypotheses. Surprisingly, CT increases PR, indicating that higher CT leads to higher demand for PR among users. This positive impact is inconsistent with the majority findings in previous research 29, 30. Nevertheless, our study stands out as one of the limited investigations providing additional evidence supporting the correlation between higher trust and increased risk perception 31. It can be implied that there is an emerging tendency to view it as a notable signal that distinguishes Gen Z from other generations. Accordingly, risk disclosure is preferable among Gen Z’s users, as they believe that an increase in trust toward technology is accompanied by a desire for awareness or information regarding risks, rather than solely focusing on perceived advantages.

Bootstrap Result

Hypothesis Testing

|

Beta (β) |

Standard Deviation |

T-statistics |

P-Values |

Remarks | ||

|

H1 |

CT → CUI |

0.65 |

0.04 |

15.78 |

0.00* |

Supported |

|

H2 |

CT → PR |

0.37 |

0.05 |

7.01 |

0.00* |

Reversely Supported |

|

H3 |

PR → CUI |

0.13 |

0.05 |

2.73 |

0.01* |

Reversely Supported |

|

H4 |

CT → PR → CUI |

0.05 |

0.02 |

2.44 |

0.01* |

Supported |

Implication and Conclusion

Based on the analysis of the previous sections, this part provides further discussion of managerial implications and subsequently provides a conclusion summarizing the study. The data highlights that three out of six major components in PR’s construct, particularly PER, TR, and SER are significant aspects in determining the continuance usage intention (CUI) of biometric authentication in digital payments. This suggests that Gen Z prioritizes biometrics performance, security level, and high speed in conducting payments. The majority of respondents are reported to have a monthly income of less than 10 million VNĐ, they might not frequently be engaging with high-value transactions, therefore explaining the reasons that FR and PYR are not major concerns for this demographic. Surprisingly, SR did not emerge as a significant item, given Gen Z’s active engagement in social communications, prompting for further research. Therefore, service providers, technicians, and managers should enhance system performance to prevent disconnections, lagging, or less sensitive circumstances.

Furthermore, the verification process should be enhanced and optimized to save time, as respondents continue to perceive it as confusing and complex. Besides implementing Law No. 26/2023/QH15 on Vietnamese biometric confidentiality, policymakers should develop AI platforms to detect fraud early and emphasize security laws related to biometric payments. Consistent with previous research 42, 43, CT is a key determinant of CUI in digital payment. Thus, improving CUI should start by enhancing CT through effective marketing campaigns and policies designed by managers and marketing experts together with appropriate policies that emphasize the trustworthiness of businesses.

Notably, this paper’s findings reflect a new tendency in user perception, such that CT positively impacts PR and subsequently enhances CUI. This implies that as a new technology emerges, a higher level of trust correlates with an increased demand for understanding perceived risks. Customers are more likely to trust technologies, particularly biometric authentication when they are aware of the associated risks. Consequently, risk disclosure is highly recommended to provide users with information related to potential risks. Through this, customers can become informed regarding the risks they may encounter and learn strategies to mitigate or address unexpected issues.

In conclusion, whilst biometric authentication usage for digital payments is increasingly adopted among Gen Z, its continuance usage intention (CUI) remains uncertain. To mitigate the possibility of alternatives, consolidating consumer trust (CT) is a crucial responsibility for stakeholders. Furthermore, businesses providing biometric authentication should clearly clarify the potential benefits and drawbacks regarding this authentication method, ensuring that users are informed rather than being vulnerable to fraud. In this context, enhancing risk literacy is vital, as it can stimulate continuance usage intention (CUI). Notably, given that Gen Z Gen Z primarily considers performance, time, and security as the three risks associated with biometric usage, suggesting that there is a growing demand for improving these elements.

Limitation and Further Research

This study focuses exclusively on Gen Z individuals residing or studying in Ho Chi Minh City. Thus future research could expand the scope by incorporating a larger and more diverse sample. Moreover, the research does not completely explain why Gen Z does not prioritize social risk (SR), despite strong engagement with social communication in their daily lives. This gap in understanding prompts further investigation to explore the factors influencing these individuals’ perceptions of social risk about biometric authentication. In addition, given this paper explores the relationship between three key variables, consumer trust (CT), perceived risk (PR), and continuance usage intention (CUI), future studies could expand by examining additional factors, such as perceived benefits and customer loyalty, providing a more comprehensive understanding of biometric authentication in online payments.

ABBREVIATIONS

GMV: Gross Merchandise Volume

PCA: Principal Component Analysis

CUI: Continuance Usage Intention

CT: Customer Trust

PR: Perceived Risk

PER: Performance Risk

FR: Financial Risk

TR: Time Risk

SR: Social Risk

PYR: Psychological Risk

SER: Security Risk

PLS-SEM: Partial Least Squares Structural Equation Modeling

CONFLICT OF INTEREST

The authors declare that there is no conflict of interest in the publication of this article.

AUTHORS’ CONTRIBUTIONS

Hoang Phuong Gia Minh is responsible for the Abstract, Literature Review, Results and Discussion, and Implication and Conclusion.

Shon Hoang is responsible for the Introduction, Background Research, Methodology, and Limitation and Further Research.