Identify factors affecting the sustainable development of micro and small-sized enterprises - A case study of Vietnam

- Thanh Dong University, Vietnam

- Ho Chi Minh City University of Economics and Finance, Vietnam

Abstract

Enterprises play a vital role in every economy, serving as the backbone of economic activities worldwide. In recent years, environmental sustainability has become an increasingly pressing global concern, affecting not just developed nations but also micro and small-sized enterprises in emerging economies. Hence, approaches to the sustainable development of enterprises are the best way to deal with the environmental impacts of natural resource depletion. Many large enterprises joined the World Business Council for Sustainable Development. In addition, micro and small-sized enterprises also pay various degrees of attention to environmental issues and sustainable operations. However, in Vietnam, the owners of micro and small-sized enterprises mainly focus on short-term business performance. This study analyzes the factors affecting the sustainable development of micro and small-sized enterprises in Vietnam based on fundamental theories such as institutional theory, stakeholder theory, and legitimacy theory. Applied quantitative research methods to analyze data collected from 211 managers at micro and small-sized enterprise managers in five centrally-governed cities in Vietnam. The hypotheses and structure equation models were tested using SmartPLS software. The results showed that Environmental, Social, and Governance (ESG) has the highest direct impact on the sustainable development of micro and small-sized enterprises in Vietnam. Meanwhile, economic development has the lowest impact on the sustainable development of micro and small-sized enterprises in Vietnam. As a result, this study indicates that enterprises and governments must understand the importance of ESG practices for sustainable development in today’s economy. It highlights the need for both enterprises and government bodies to recognize and prioritize ESG principles to foster a more sustainable and inclusive economic future. By doing so, they can develop strategies that promote the long-term viability of domestic enterprises.

INTRODUCTION

In the context of declining natural resources, environmental degradation and especially the impact of the COVID-19 pandemic, sustainable development has become a goal that countries want to achieve. Sustainable development relates to meeting current needs without compromising or harming the ability of future generations to meet their needs1. In other words, sustainable development is the overarching concept of three crucial pillars of economy, society and environment2.

Recently, sustainable development has been spreading at the enterprise level3. It is a common trend for enterprises globally towards sustainable development goals because they play a crucial role in the national economy, especially their central position in human development4. Sustainable enterprise development reflects the level of enterprises promoting social, economic and environmental development activities5.

In Vietnam (an emerging economy in Southeast Asia), micro and small-sized enterprises account for more than 80 per cent of enterprises, with about 1.7 million enterprises creating the most jobs and contributing more than 40 per cent of GDP per year6. These contributions supported economic, social, environmental, poverty alleviation, and social justice programs. However, in the context of many new challenges, especially the impact of climate change, it is becoming increasingly difficult to achieve sustainable development of micro and small-sized enterprises in Vietnam7.

The study of Nguyen and Nguyen used the triple bottom line-3BL theory as an analytical framework for the sustainable development of small and medium-sized enterprises in Vietnam8. Or Nguyen and Tran based on the theory of planned behavior, identified four factors that affect the sustainable business of small and medium-sized enterprises in Vietnam, including attitudes, ethical standards, perceived desires, and corporate culture9. Thus, although the sustainable development of enterprises has been studied, these research models have not comprehensively explained the factors affecting the sustainable development of micro and small-sized enterprises in Vietnam. Therefore, this study is carried out based on inheriting and perfecting several quantitative research models on enterprise sustainability that have been empirical in the world, as well as proposing and testing models to measure the impact of factors on the sustainable development of enterprises consistent with the practices of micro and small-sized enterprises in Vietnam. In particular, this study considered the term “ESG” as a crucial facet of the sustainable development of micro and small-sized enterprises in a developing country like Viet Nam.

This article is organized as follows. Section 2 presents a literature review and hypothesis development. Section 3 describes the methodology. Section 4 presents the crucial findings and discussions. Section 5 is the conclusion, implications, limitations, and suggestions for further research.

LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT

Underpinning theory

Institutional theory

According to North, institutions are human constraints that shape political, economic, and social interactions10. They include informal (prohibitions based on customs, traditions and community codes of conduct) and formal (constitutional, legislative, legal regulations and property rights. This theory also shows that the political and legal framework creates the basic principles and rules for the functioning of individuals and enterprises, voluntary and cooperative arrangements between actors that affect the exchange of cultural values and beliefs. As a result, influencing the behavior of individuals and organizations through institutional influence leads to a willingness to participate and abide by principles and rules.

Stakeholder theory

Stakeholder theory was first used by Freeman11 in 1984 in his strategic management work12. Stakeholders include any person or group of people interested in the enterprise because they may be affected by its operations13. This theory refers to ethics and values in organizational governance. Stakeholders expect enterprises to behave consistenty with their responsibilities to achieve legitimate society activities that will help them gain other economic benefits.

Legitimacy theory

Legitimacy theory is rooted in the concept of organizational legitimacy. It is a condition or state of existence when an entity's value system matches the value system of the large social system of which the entity is a part14. According to Donaldson and Preston, legitimacy is the conformity between institutional actions and social values, while legalization is actions that organizations take either to signal conformity to values or to change social values. Legitimacy is achieved by demonstrating that the enterprise's activities are consistent with social values15.

Research concepts

Sustainable development

The term “sustainable development” has existed since the 1980s due to the World Conservation Union (WCU). In 1987, the World Commission on Environment and Development (WCED) stated that the goal of protecting natural resources requires sustainable exploitation and use. Sustainable development is the process of development that meets the needs of the present while ensuring the integrity of natural resources to meet the needs of future generations16. Sustainable development is defined based on three main pillars including:

-

Economic pillar: rapid economic growth, ensuring safety and quality.

-

Social pillar: social justice and human development, in which the human development index is the highest criterion demonstrating social development, for example per capita income, intellectual level, education, health, life expectancy, cultural enjoyment level, civilization.

-

Environment pillar: rational exploitation and use of natural resources, environmental protection and habitat quality improvement..

Enterprise sustainability

Based on the concept of sustainable development, from a business perspective, enterprise sustainability is the satisfaction of the needs of business stakeholders. Still, it does not detract from the interests of future stakeholders. Enterprise sustainability focuses on strategies and operational directions of ones according to three core pillars including economy, society and environment17.

The study of Lo identified enterprise sustainability as a process that integrates aspects including financial benefits, environmental protection and social responsibility in business operations and governance18. However, van Marrewijk emphasized that there is no fixed concept of enterprise sustainability, since approaching the process of sustainable development must depend on many internal factors such as organizational structure, mode of operation, enterprise purpose and so on19.

Enterprises need to develop sustainable development strategies linked to their business models, using new strategies, governance performance and stakeholder engagement conscientiously to continuously improve economic, environmental and social conditions on a regional and global scale20.

In summary, although there are different perspectives on enterprise sustainability21, 22, 23, but the similarities are all directed at the concern for the three pillars of economy, environment, and society, and they are systematically linked together at different levels that enterprises wish to address simultaneously.

Hypothesis development

Bansal approached the concept of sustainable development in general and the sustainable development of enterprises in particular by exploring fundamental theories such as institutional theory, stakeholder theory, and legitimacy theories. He proposed that for an enterprise to pursue the trend of sustainable development, it is necessary to fully integrate three factors: economy, society, and environment. Without any of these factors, enterprises cannot achieve sustainable development24. Supporting this opinion, Lee and Sean found a close connection between economic, social, and environmental development factors and sustainable breakthroughs25. These three factors are explained as follows:

i) Economic development is a prerequisite for the survival or failure of enterprises. Most enterprises aim for economic development to establish a position in the market. The economic development of an enterprise is assessed through its level of growth, scale of production and business, and long-term profits. It involves achievements related to financial success and crucial contributions to the national and local economy. Thus, economic development encompasses expanding production and business activities, achieving financial growth, strengthening the enterprise’s market position, and creating success for the enterprise.

ii) Social development involves minimizing the negative impacts of the enterprise on the community and the environment where it operates while strengthening social relationships with stakeholders directly related to the enterprise, including employees, local communities, customers, suppliers, and government. Additionally, the enterprise should aim for honesty and transparency in its production and business activities, comply with legal regulations, uphold business ethics, create conditions for human development, promote creativity and innovation, and ensure fairness and respect for the common interests of society. The enterprise also participates in community support activities such as education, health, poverty alleviation, infrastructure development, and focuses on the health of customers and employees. Thus, social development represents the responsibility of enterprises in achieving social improvement goals.

iii) Environmental development involves using corporate governance methods to minimize environmental impact, reduce the use of natural resources and fossil fuels, and minimize emissions. Additionally, enterprises should apply green technologies to manage, protect, and improve environmental quality; promote green consumption and green payment practices; and develop detailed environmental development plans to prevent potential pollution risks. This includes recycling waste and products to reduce impact on the ecological environment. Therefore, environmental development is the process by which enterprises engage in environmental protection activities while still achieving economic benefits and maintaining efficiency in production and business operations.

Several domestic and foreign studies, using qualitative and quantitative research methods, have revealed that without one of the three factors of economic, social, and environmental development. It is pretty difficult for enterprises to increase competitiveness and develop sustainably. These three factors are always considered fundamental for businesses aiming to develop sustainably in the future26, 27, 7. Based on the argument above, hypotheses are proposed as follows:

H1: Economic development will be positively associated with enterprise sustainability

H2: Social development will be positively associated with enterprise sustainability

H3: Environment development will be positively associated with enterprise sustainability

Schein suggested that enterprise culture is the foundational factor that shapes the behaviors and activities of each employee, serving as a unique intangible product of each organization28. Kotter and Heskett proposed that enterprise culture consists of a set of intertwined values and behaviors that commonly occur within enterprises and tend to spread and persist over time29. Pham described enterprise culture as a synthesis of values and both material and spiritual assets created during the formation, operation, and development of enterprises. These values influence and govern the thinking and behavior of employees30. Nguyen et al. proved that enterprise culture is one of the essential factors for businesses to conduct sustainable business31. In the industrial revolution 4.0, if enterprises want to develop sustainably, they need to determine the leading role of enterprise culture9. Based on the argument above, hypotheses are proposed as follows:

H4: Enterprise culture will be positively associated with enterprise sustainability

Brand identity is expressed through image design, image positioning or expression of the physical form of the organization through the logo and colors of the enterprise32. Brand identity is the authentication of the existence, activities and business behavior of an enterprise33. Brand identity is used to find the differences between enterprises, and it is reflected in the core characteristics and long-term orientation of ones34. Alcívar et al. emphasized that an appropriate brand identity policy will help enhance the image and create crucial impacts on enterprise sustainability in the long run27. In other words, brand identity is one factor that motivates businesses to easily achieve sustainable development goals7. Green brand identity generally involves building an enterprise’s reputation and creating an environmentally friendly image through activities or commitments to environmental protection during business operations. These activities include using environmentally friendly materials, ensuring that all products meet environmental standards or can be recycled, saving energy and resources, minimizing emissions, communicating about environmental protection initiatives, supporting community environmental efforts, and so on. Thus, green brand identity is an important lever to help enterprises approach the sustainable development process more quickly and drastically. Based on the argument above, hypotheses are proposed as follows:

H5: Green brand identity will be positively associated with enterprise sustainability

The precursor to ESG (Environment, Social and Governance) was corporate social responsibility (CSR), which first appeared in a book by Bowen35. The term ESG (Environment, Social and Governance) first appeared in a United Nations Global Compact report in late 2004 titled “Who Cares WIN Connecting Finance Marketing to a Changing World”. At the time, the report highlighted the need for responsible investment, considering environmental, social and governance factors. ESG is explained as follows:

-

E - Environmental: a group of standards that measure the level of a business's impact on the environment and natural resources. For instance, reducing carbon emissions and maintaining the sustainability of physical assets; reducing pollution of soil, water, air, and other types of pollution; effectively reducing, treating, and recycling waste; and efficiently using resources and energy. An enterprise focusing on ESG implementation can consider appropriate actions to both ensure business operations and protect the environment36.

-

S - Social: The standards group measures factors related to relationships both inside and outside the business, including relationships with partners, customers, and employees. For instance, focusing on improving the basic needs, working environment, welfare, and career opportunities of employees; providing quality products and services; ensuring the privacy and security of customer information; and ensuring sustainable business models and products that are accessible and beneficial to the community36.

-

G - Governance: A group of standards that measure efficiency, transparency, business ethics, and compliance with local regulations in business operations. For instance, , they should adhere to ethical principles in business; ensure transparency in the disclosing information related to business activities; protect intellectual property rights; select the board of directors responsibly; and be accountable to shareholders. The enterprise must be transparent, accurate, and fair in selecting board members. At the same time, measures should be taken to combat bribery and corruption in the process of corporate governance36.

Thus, the essence of ESG is the measurement and evaluation based on three key factors that are directly related to the sustainable development of the enterprise. In addition, recent recommendations suggest that ESG needs to be integrated with the business strategy of enterprises and become the main orientation for enterprises to implement development plans geared towards green and sustainable growth, effective use of resources, and enhanced social and community responsibility. To develop sustainably, enterprises must meet the criteria set by ESG. Therefore, ESG is considered a fundamental factor affecting the sustainable development of enterprises. Based on the argument above, hypothesis are proposed as follows:

H6: ESG will be positively associated with enterprise sustainability

The research model is illustrated in Figure 1.

Research Model

RESEARCH METHODS AND DATA

Scale

The scales are inherited from domestic and foreign studies by Bansal24, Chow and Chen26, Alcívar et al.37, Sinha et al.36, Tran7, Nguyen et al.9. We use a 5-degree Likert scale with 1 - strongly disagree, 3 - neutral, 5 - strongly agree.

This study was conducted in Vietnam, which is a developing country, but the initial scale was mainly verified in developed countries. So, the discovery study was conducted through in-depth interviews with experienced experts in the field of sustainable development and group discussions with target respondents (five micro and small-sized enterprise owners) using a purposeful sampling method to ensure that it is consistent with the practical context in Vietnam in general and the five cities selected for the survey in particular. The discovery results showed that experts and target respondents agreed on the scales and items in the proposed research model. Nevertheless, when translated from the original English questionnaire into Vietnamese, some items have been worded to be consistent with the grammar of Vietnamese people (see Table 1).

Before conducting the formal survey, the authors conducted a preliminary study of 35 micro and small-sized enterprise owners to check their reliability and adjust the formal scale again. The results showed that the Cronbach's Alpha coefficient of the scales all exceeded the threshold of 0.7 and the Corrected Item - Total Correlation was more significant than 0.4. Thus, the scales met the conditions for conducting the formal survey.

Data collection

Managers at micro and small-sized enterprises in five centrally-governed cities (Hai Phong, Hanoi, Da Nang, Ho Chi Minh and Can Tho Cities) were selected for this study using a convenient non-probability sampling method. Since they are Vietnam's most critical economic development localities, more than 80 per cent of the country's operating enterprises are concentrated in these areas. The minimum sample was 240 samples according to the formula of Hair et al. (2016) with a significance level of 1 per cent. Still, after cleaning, the formal sample size for analysis was 211 samples, a rate of 87.9 per cent. The survey was conducted online via Google form for 16 weeks (from January to April 2024). Of the 211 respondents, 75.3 per cent were male, and 24.7 per cent were female. The respondents were service enterprises accounting for 54 per cent, and manufacturing enterprises accounting for 36.5 per cent, most of which operate with a capital of less than VND 50 billion. Additionally, the number of employees working at enterprises between 51 and 100 employees accounts for 45 per cent and from 11 to 50 employees accounts for 24.6 per cent. 42.2% of enterprises operate from 6 to 10 years and from 1 to 5 years, accounting for 36.5%.

Data analysis

This study used partial least square-structural equation modeling (PLS-SEM) to analyze data through the SmartPLS 4.0 program. Data analysis includes the measurement model (reliability, convergent validity, discriminant validity) and structural model.

FINDINGS AND DISCUSSION

Measurement model

Table 1 describes the items for the structural model and summarises the results of the analysis of reliability and convergent validity. The analysis results showed the outer loadings exceeding 0.4 (p < 0.05), the average variance extracted (AVE) over threshold 0.5. Cronbach’s Alpha value and composite reliability (CR) exceed the threshold of 0.7 suggested by Hair et al.. So, the constructs achieve internal consistency reliability.

The results of the reliability and convergent validity

|

Items |

Sign |

Cronbach’s α, CR, AVE |

λ |

Source |

|

Economic development (Eco) | ||||

|

Enterprises make maximum use of waste in business operations to minimize costs |

Eco4 |

0.896 0.911 0.620 |

0.807 |

Chow and Chen |

|

Enterprises minimize unimportant input costs to focus on developing output products |

Eco5 |

0.741 | ||

|

Enterprises comply with requirements and legal documents of State management agencies in business operations to maintain growth |

Eco6 |

0.796 | ||

|

Enterprises cooperate with research institutes to apply modern technologies to improve productivity and quality in business operations |

Eco3 |

0.772 | ||

|

Enterprises implement marketing strategies with the aim of making a difference to achieve profits and drive business efficiency |

Eco1 |

0.743 | ||

|

Enterprises diversify product categories to meet customer needs to increase revenue and ensure development |

Eco2 |

0.819 | ||

|

Social development (Soc) | ||||

|

Enterprises focus on the health and safety of employees and the local community during business operations |

Soc1 |

0.835 0.849 0.700 |

0.723 |

Chow and Chen |

|

Enterprises actively participate in projects that support local community development |

Soc3 |

0.800 | ||

|

Enterprises protect the rights and act in the interests of the local community |

Soc5 |

0.711 | ||

|

Enterprises are willing to disclose the impacts and risks that will occur to the environment to the local community |

Soc4 |

0.868 | ||

|

Enterprises have direct dialogue with the local community before making investment decisions |

Soc2 |

0.782 | ||

|

Environment development (Env) | ||||

|

Enterprises seeking to reduce the use of fossil energy sources and emissions in their business operations |

Env4 |

0.881 0.904 0.603 |

0.825 |

Chow and Chen |

|

Enterprises seek to use materials that are less polluting to the environment and can be recycled |

Env1 |

0.757 | ||

|

Enterprises seeking to minimize the impact of products, goods or services on the natural environment |

Env6 |

0.833 | ||

|

Enterprises build and install wastewater treatment systems to protect the environment |

Env7 |

0.739 | ||

|

Enterprises aim to protect the environment along with economic benefits |

Env5 |

0.764 | ||

|

Enterprises sponsor and respond to local environmental protection activities |

Env8 |

0.805 | ||

|

Enterprises comply with regulations and participate in training courses on environmental protection of local authorities |

Env2 |

0.830 | ||

|

Enterprises develop plans and set aside funds to respond to environment-related incidents |

Env3 |

0.783 | ||

|

Enterprise culture (EC) | ||||

|

Mission, vision and core values of the enterprise towards green development and growth |

EC5 |

0.801 0.817 0.542 |

0.728 |

Nguyen et al. |

|

Enterprises implement training courses on environmental protection to raise employees’ awareness of environmental matters |

EC1 |

0.837 | ||

|

Enterprises encourage employees to improve their professional qualifications and competencies |

EC2 |

0.809 | ||

|

Enterprises focus on improving the internal and external working environment of employees |

EC4 |

0.813 | ||

|

Enterprises propagating and organizing movements to respond to environmental protection |

EC6 |

0.748 | ||

|

Enterprises promulgate regulations on standard culture and behavior in the working process |

EC3 |

0.777 | ||

|

Green brand identify (GBI) | ||||

|

Enterprises build an environmentally friendly image |

GBI1 |

0.792 0.799 0.591 |

0.760 |

Alcívar et al. |

|

Enterprises promote and position green brands in the hearts of customers |

GBI3 |

0.854 | ||

|

Enterprises focus on developing products with environmental protection characteristics |

GBI2 |

0.861 | ||

|

Businesses use blue tones as the main color |

GBI4 |

0.872 | ||

|

Environment, Social and Governance (ESG) | ||||

|

Enterprises replace equipment, tools, machinery, offices and factories with environmentally friendly materials |

ESG4 |

0.906 0.914 0.685 |

0.709 |

Sinha et al. |

|

Enterprises maximize the application of technology in the working process to minimize operating costs |

ESG8 |

0.717 | ||

|

Enterprises care and treat employees fairly |

ESG3 |

0.808 | ||

|

Enterprises respect confidentiality and are willing to provide benefits and risks of products and services to customers |

ESG6 |

0.791 | ||

|

Enterprises listen to feedback from employees and customers |

ESG7 |

0.793 | ||

|

Enterprises encourage employees to use environmentally friendly items |

ESG2 |

0.784 | ||

|

Enterprises ensure working conditions and compliance with legal regulations for employees |

ESG1 |

0.843 | ||

|

Enterprises publicize annual business results |

ESG5 |

0.826 | ||

|

Enterprises take measures to prevent negative behaviors arising in business activities |

ESG9 |

0.758 | ||

|

Enterprise sustainability (ES) | ||||

|

Enterprises want to develop sustainably in the future |

ES |

- |

1,00 |

The authors |

In addition, this study found that the square root values of the AVE coefficient range from 0.736 to 1.00, and they are more significant than the correlation between the factors. At the same time, the HTMT correlation index does not exceed the threshold of 0.85 and is less than CR (see Table 2). Thus, the results indicated that the constructs are reliable, convergent and discriminant and can be used to evaluate structural models38, 39.

The result of discriminant validity

|

Soc |

Eco |

Env |

EC |

GBI |

ESG |

ES | |

|

Soc |

0.836 | ||||||

|

Eco |

0.562 0.573 |

0.787 | |||||

|

Env |

0.695 0.707 |

0.288 0.291 |

0.776 | ||||

|

EC |

0.208 0.213 |

0.712 0.717 |

0.633 0.636 |

0.736 | |||

|

GBI |

0.324 0.329 |

0.403 0.416 |

0.189 0.192 |

0.409 0.411 |

0.769 | ||

|

ESG |

0.581 0.586 |

0.590 0.600 |

0.088 0.094 |

0.117 0.122 |

0.662 0.671 |

0.827 | |

|

ES |

0.622 0.630 |

0.444 0.448 |

0.375 0.382 |

0.223 0.225 |

0.227 0.230 |

0.354 0.355 |

1.00 |

Structural model analysis

Table 3 shows the VIF values don’t exceed the threshold 5 so the structure model does not have multicollinearity. Additionally, the f values are more than 0.2 so the independent variables have a high effect size on the dependent variable in the research model40.

The values VIF and f2

|

Hypothesis |

VIF |

f2 |

|

H1 |

3.219 |

0.321 |

|

H2 |

2.543 |

0.432 |

|

H3 |

2.110 |

0.355 |

|

H4 |

4.206 |

0.367 |

|

H5 |

1.943 |

0.412 |

|

H6 |

2.704 |

0.501 |

Table 4 also shows R value has an appropriate predictive power since the endogenous latent variable “Enterprise sustainability” exceeds the threshold of 0.5 recommended by Hair et al.40. Moreover, the analysis results also found Q > 0, so the structural model achieved overall quality.

The values R2 and Q2

|

R2 |

R2 adjust |

Q2 | |

|

ES |

0.746 |

0.733 |

0.594 |

Besides, we conducted Bootstrap 5000 times40 to consider the value of the standardized impact factor (β), the significance level (p), and the value of the test t.

Results of the hypothesis test

|

Hypothesis |

β |

SD |

t |

Conclusion |

|

H1 |

0.487 |

0.017 |

4.003** |

Accepted |

|

H2 |

0.514 |

0.023 |

2.876** |

Accepted |

|

H3 |

0.493 |

0.024 |

5.553** |

Accepted |

|

H4 |

0.556 |

0.015 |

3.985** |

Accepted |

|

H5 |

0.572 |

0.022 |

4.691* |

Accepted |

|

H6 |

0.601 |

0.020 |

5.124* |

Accepted |

|

χ2 = 742.371 (p < 0.05), df = 632 χ2 /df = 1.454, GFI = 0.887, NFI = 0.895, TLI = 0.909, CFI = 0.911, RMSEA= 0.068 Notes: * significant at p < 0.05; ** significant at p < 0.01 | ||||

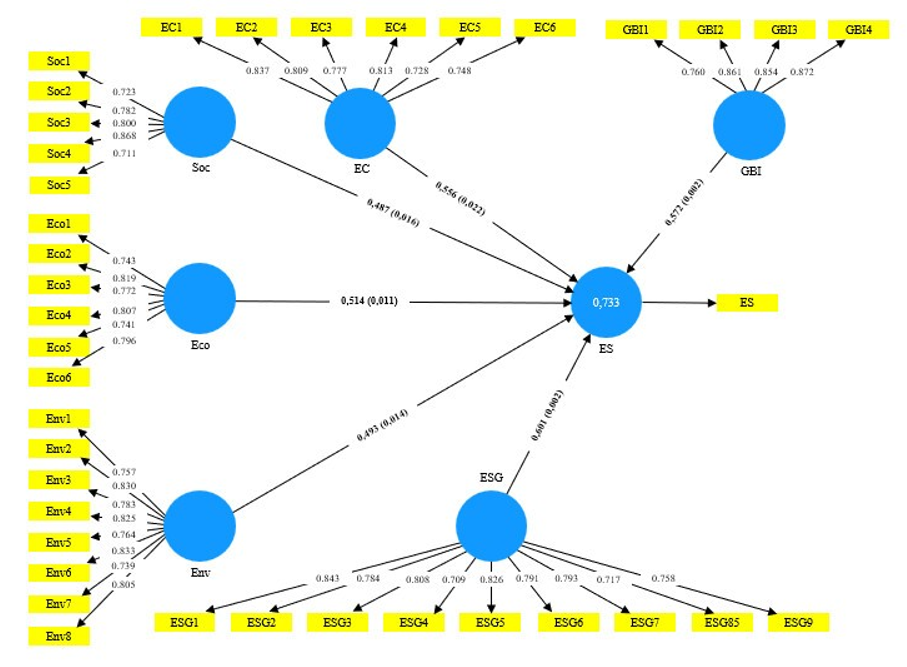

PLS-SEM showing positive relationships in variables (Source: Authors’ analysis)

Table 5 and Figure 2 confirm that the proposed research hypotheses are accepted. Independent factors (Eco, Soc, Env, EC, GBI, ESG) have a positively impact on the dependent factor “Enterprise sustainability”. The factor of ESG has the highest impact, while the factor of social development has the lowest impact on the sustainable development of micro and small-sized enterprises.

Discussion

In this study in Vietnam, six factors directly affect enterprise sustainability: economic development, social development, environment development, enterprise culture, green brand identity, and ESG. The results of the study are similar and different from those of previous studies.

To begin with the H1 hypothesis, economic development positively impacts enterprise sustainability. This finding is similar to the study of Chow and Chen. Economic development opens up opportunities for profit growth and business scale for micro and small-sized enterprises. As the economy grows, micro and small-sized enterprises have better financial capacity to invest in technology, human resources, and sustainability initiatives.

Next, unraveling the H2 hypothesis, social development positively impacts enterprise sustainability. This result is consistent with the findings of Chow and Chen. In fact, Vietnamese micro and small-sized enterprises have also begun to be more aware of their role in contributing to the development of society through activities such as supporting education, health, environmental protection and the community, which have contributed to improving the image and reputation of enterprises, at the same time, creating sustainable value for both enterprises and society.

Next up, the H3 hypothesis is that environmental development positively impacts enterprise sustainability. This finding is similar to the study of Chow and Chen26. In fact, environmental development encourages enterprises to use natural resources effectively and sustainably. Currently, many enterprises have applied measures to save energy, manage waste and use renewable resources to reduce production costs, increase business efficiency and protect the environment.

Regarding the H4 hypothesis, enterprise culture positively impacts enterprise sustainability. This finding is similar to the study of Nguyen et al.31. Enterprise culture promotes long-term vision instead of focusing only on short-term benefits. Currently, micro and small-sized enterprises are tending to invest in sustainable activities, from resource management to human resource development, as a result creating a solid foundation for the sustainable development of the enterprise.

Next, the H5 hypothesis is that green brand identity positively impacts enterprise sustainability. This result is consistent with the findings of Tran7. Currently, consumer trends are shifting towards eco-friendly products and services. A green brand identity is a tool for micro and small-sized enterprises to meet the growing market demand for sustainable products due to expanding the market and increasing sales.

Finally, the H6 hypothesis states that ESG has positive enterprise sustainability. This finding is the highlight of our study. So far, no formal study in Vietnam has proven the relationship between ESG and enterprise sustainability. Nowadays, investors are increasingly interested in ESG factors when making investment decisions. Micro and small-sized enterprises with good ESG practices attract more investors, since they are less risky and have the potential for sustainable development. Besides, ESG practices contribute to building and improving corporate reputation and image. Enterprises with social and environmental responsibility are more appreciated by consumers, communities and stakeholders, thereby increasing their profits.

Theoretically, the findings of this study are consistent with institutional theory10, stakeholder theory11, and legitimacy theory14 in explaining the factors that affect enterprise sustainability. The Least Squares Structural Equation Modeling (PLS-SEM) has also accepted the proposed factors. This provides empirical evidence that economic development, social development, environment development, enterprise culture, green brand identity, and ESG are positively related to the sustainable development of micro and small-sized enterprises in Vietnam – a developing country.

Practically, the research results are a crucial signal for managers of Vietnamese micro and small-sized enterprises to pay special attention to the aspects of economic development, social development, environmental development, enterprise culture, green brand identity, and ESG to build enterprise sustainability.

CONCLUSION

Based on empirical data and insights from previous studies, our study highlights the crucial impact of economic development, social development, environment development, enterprise culture, green brand identity, and ESG in achieving enterprise sustainability. And we've also expanded on the scant documentation of these constructs. Although the literature on the construct relationships in this study is increasing, this study provides more concrete evidence in the context of an emerging economy. Besides, this study considered ESG to be a crucial factor in enterprise sustainability.

In addition to the results achieved, the study still has several limitations as follows:

Firstly, this study has only focused on collecting data from micro and small-sized enterprises in five centrally-governed cities, so the scope is not wide. So, future studies should expand the scope to other localities to increase the sample size and generality.

Secondly, the results of this study are based on causal model analysis with cross-sectional data. It is not optimal because the chronological order of the construct, one of the crucial factors in causal modeling analysis is omitted. Future studies should collect a time series, and cross-sectional data aggregated for investigation, or the studies can be designed vertically to collect data at different times, and the results of this research design can clearly describe the changing patterns and the extent of the causal relationship between the variables.

ABBREVIATIONS

AVE: Average Variance Extracted

CR: Composite Reliability

CSR: Coporate Social Responsibility

ESG: Environmental, Social, and Governance

GDP: Gross Domestic Product

HTMT: Heterotrait-monotrait

CONFLICT OF INTEREST

The authors declare that they have no conflicts of interest.

AUTHORS’ CONTRIBUTION

Nguyen Danh Nam: conceptualization

Nguyen Danh Nam, Uong Thi Ngoc Lan and Nguyen Minh Ngoc: data collection and curation

Nguyen Danh Nam, Uong Thi Ngoc Lan and Nguyen Minh Ngoc: formal analysis

Nguyen Danh Nam: methodology

Uong Thi Ngoc Lan: writing - original draft

Nguyen Danh Nam and Uong Thi Ngoc Lan: writing - review & editing