The moderating role of managerial support in the perception of IFRS and preparedness for IFRS application

- Industrial University of Ho Chi Minh City, Vietnam

Abstract

This study investigates how manager support moderates the relationship between the perception of IFRS and preparedness for IFRS application. A survey of 238 large companies in Southern Vietnam was conducted from November 2021 to March 2022, and partial least squares structural equation modeling (PLS-SEM) was used to analyze the data. The findings of this study indicate that perceptions of benefits and managerial support positively influence preparedness for IFRS application. Conversely, perceptions of challenges and disadvantages are negatively associated with preparedness for IFRS adoption. Furthermore, manager support moderates the negative relationship between perceived challenges and preparedness for IFRS application. However, the study does not find that managerial support moderates the impact of perceptions of disadvantages or benefits on preparedness for IFRS application. This study contributes to applying agency theory in the context of IFRS adoption. The finding provides insights into how the perception of IFRS can affect the agency relationship between managers and shareholders and how managerial support can moderate this relationship. The research findings enhance our comprehensive understanding of how manager support moderates the relationship between IFRS perception and preparedness for IFRS application. This insight holds particular significance for large firms, as they commonly encounter challenges and constraints in this context. Managers can enhance IFRS application by implementing appropriate policies that promote a positive perception of IFRS and increase managerial support. However, a limitation of this study is that it relates to data collected primarily from large firms in Southern Vietnam. Expanding the study to include diverse regions could help explore regional variations. Future research in different countries could assess cross-cultural differences in IFRS preparedness and consider additional variables, such as firm characteristics and industry type, for a more comprehensive understanding.

Introduction

IFRS (International Financial Reporting Standards) application offers numerous benefits and advantages for companies, as demonstrated by several studies1, 2, 3, Daske, Hail 4, 5. Florou and Kosi 6 illustrated an overall increase in market liquidity and decreased cost of capital associated with IFRS adoption. Consequently, the IFRS application has garnered significant research interest worldwide.

Previous research on IFRS application has primarily focused on three key areas. Firstly, studies have delved into the factors influencing IFRS adoption, with research by Chung and Park7, Di Fabio 8, and Amano9 shedding light on various aspects. For instance, Sato and Takeda 10 demonstrated the negative impact of financial leverage on IFRS adoption, while Alanezi and Albuloushi11 found that profitability negatively affects the willingness of listed companies to apply IFRS. Secondly, researchers have explored the advantages of IFRS implementation, as exemplified by studies conducted by Kim, Tsui and Yi12, Bertrand, de Brebisson and Burietz 13, and Cameran and Campa 14. Gassen and Sellhorn 15 contended that IFRS adoption enhances earnings quality and reduces information asymmetry due to its stringent disclosure requirements in corporate financial statements. Thirdly, research efforts have assessed both the benefits and drawbacks of IFRS for businesses, as evidenced by the work of Doan, Thi and Phan 16, Phan, Joshi and Mascitelli 17, Phan18, and Guerreiro, Rodrigues and Craig 19. These investigations have often focused on economies either preparing for IFRS adoption or undergoing a gradual integration process.

As proposed by Watts and Zimmerman20, ositive accounting theory aims to explain and predict the reasons behind the acceptance of accounting policies. This theory suggests that companies choose their accounting standards based on their perceptions21. According to positive accounting theory, managers are primarily motivated by self-interest to maximize their own utility. Consequently, when managers perceive positive outcomes resulting from IFRS adoption, such as improved financial reporting quality or enhanced investor confidence, they tend to support and advocate for adopting IFRS within the organization. However, previous studies have not explored the role of manager’s support in moderating the relationship between the perception of IFRS and preparedness for IFRS application. To address this gap, the author surveyed 238 respondents to investigate how manager’s support influences the link between the perception of IFRS and preparedness for IFRS application. The empirical research findings indicate that manager’s support can mitigate the negative impact of perceived challenges on preparedness for IFRS application.

Theoretical Background and Hypothesis

Perception of IFRS and preparedness for IFRS application

Tokar22 examined the challenges of IFRS application, which are relative to barriers encountered during the conversion stage of firms. Parvathy 23 argued that challenges in the IFRS application process include the scarcity of resources and a lack of experts in enterprises. Anh, Thi and Tu 24 suggested that language barriers and difficulty in recruiting accounting staff are significant challenges during the IFRS application in Vietnam. Phan, Joshi and Mascitelli 17 confirmed that the perceived challenges of IFRS have a negative impact on the willingness to adopt IFRS. Organizations may need to allocate additional resources, both financial and human, to address the perceived challenges of implementing IFRS 25. The perception of these resource requirements can influence their readiness or preparedness, as they need to plan and budget accordingly. Moreover, IFRS implementation requires specialized knowledge and expertise that the organization currently lacks, which can impact preparedness 26. Organizations might need to invest in training or hiring experts, which can be a time-consuming and costly process 27. The perception of challenges might include concerns about the technical infrastructure needed for IFRS reporting 25. Based on the literature review above, the author proposes the first hypothesis as follows:

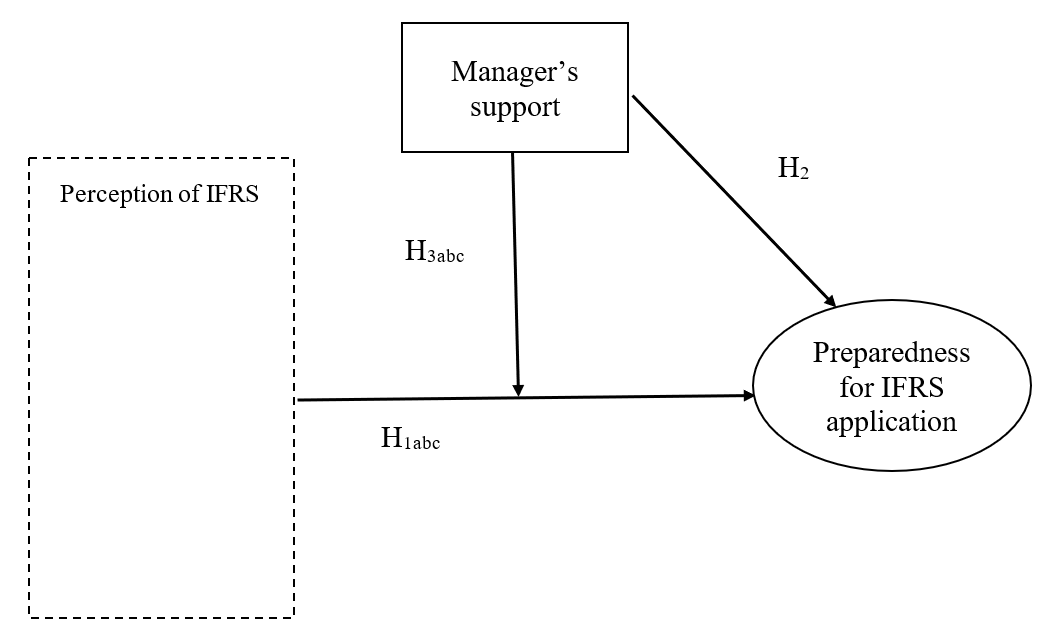

Hypothesis H1a: The perception of challenges is positively associated with preparedness for IFRS application.

Armstrong, Barth 3 stated that IFRS application in enterprises not only increases costs but also raises the mobilization costs of firms. IFRS application can reduce replacement options, leading to a less honest presentation of corporate operations 28. Hu29 confirmed that managers in Japan perceive more disadvantages than benefits during IFRS application. The perception of higher implementation costs, including software upgrades, training, and potential consulting fees, can deter organizations from fully committing to IFRS adoption 30. If organizations perceive IFRS as overly complex or challenging to comply with, they may hesitate to undertake the transition31. Concerns about reporting and financial statement preparation complexities can impact preparedness32. Organizations might worry that transitioning to IFRS could lead to errors or financial misstatements due to unfamiliarity with the standards 33. This fear of inaccurate financial reporting can hinder preparedness. Based on this analysis, the author argues that perceiving disadvantages leads to preparedness for IFRS application. Therefore, this study proposes the second research hypothesis:

Hypothesis H1b: The perception of disadvantages is positively associated with preparedness for IFRS application.

Bassemir and Novotny‐Farkas 34 confirmed that applying IFRS allows private firms to improve the quality of earnings management. Applying IFRS increases earnings management, M&A activities, information quality, and financial performance 35. Gassen and Sellhorn15 suggested that applying IFRS increases the quality of income and decreases asymmetrical information. Applying IFRS also increases the suitable value of financial databases36, 37. Organizations may perceive that IFRS adoption can lead to more transparent and accurate financial reporting38. The belief that IFRS will enhance the quality of their financial statements can motivate preparedness efforts39. The perception is that IFRS compliance is a global standard that can improve access to international markets and investors can drive preparedness 40. Organizations may perceive that adopting IFRS will make it easier to compare their financial performance with industry peers and competitors 41. This comparability can be seen as a competitive advantage. Based on this analysis, the author argues that the perception of benefits leads to preparedness for IFRS application. Therefore, this study proposes the third research hypothesis:

Hypothesis H1c: The perception of benefits is positively associated with preparedness for IFRS application.

Manager’s support and preparedness for IFRS application

Previous studies have examined the impact of ownership structure on IFRS application. Renders and Gaeremynck42 confirmed that ownership structure is negatively associated with IFRS application. Alanezi and Albuloushi11 argued that family members o the firm board have a negative impact on IFRS application. Moreover, managers who support IFRS adoption are more likely to allocate the necessary resources, both financial and human, to ensure a smooth transition 31. This includes budgeting for training, software upgrades, and expert assistance. Moreover, transitioning to IFRS often requires changes in business processes and financial reporting practices 31. Managers can facilitate change management by communicating the benefits, setting expectations, and addressing employee concerns 37. When managers align IFRS adoption with the organization's strategic goals and vision, it reinforces the importance of the transition43. Managers play a crucial role in communicating the reasons behind IFRS adoption and its potential benefits to both internal and external stakeholders 44. Managers can ensure that employees receive the necessary training and development opportunities to acquire the skills needed for IFRS compliance 45. Drawing upon this analysis, the author contends that manager support fosters preparedness for IFRS application. Consequently, this study advances the fourth research hypothesis:

Hypothesis H2: Manager’s support is positively associated with preparedness for IFRS application.

The moderating effect of manager’s support on the relationship between perception of IFRS and preparedness for IFRS application

The viewpoint of agency theory argues that corporate governance motivations focus on the conflict between owners and managers46. According to Muth and Donaldson 47, ownership has increased the power of managers. Consequently, managers often make decisions that align with their own interests 47. Additionally, agency theory emphasizes clear accountability to the company's board and serves as a monitoring mechanism to reduce information asymmetry, thereby improving information quality48. Therefore, managers can moderate the effect of manager support on the relationship between the perception of IFRS and preparedness for IFRS application for several reasons. When managers actively support the transition to IFRS, it can amplify the positive perception of IFRS within the organization49. Employees may be more receptive to the changes and more motivated to prepare for IFRS adoption because they see it as a priority supported by leadership50.

On the other hand, when managers provide strong support, they can help mitigate negative perceptions or concerns regarding IFRS51. Managers can address employee doubts, clarify misconceptions, and provide reassurance, leading to higher preparedness levels. Moreover, a manager’s support can influence the allocation of resources to address the challenges associated with IFRS adoption 44. Managers are supportive, they are more likely to allocate resources to training, system upgrades, and expert assistance, which can enhance preparedness 52. Overall, manager’s support can moderate the relationship between the perception of IFRS and preparedness for IFRS application. Specifically, the relationship becomes stronger when the manager’s support is high. Therefore, the author proposes the final research hypothesis as follows:

Hypothesis H3a: Manager’s support moderates the relationship between perception of challenges and preparedness for IFRS application.

Hypothesis H3b: Manager’s support moderates the relationship between perception of disadvantages and preparedness for IFRS application.

Hypothesis H3c: Manager’s support moderates the relationship between perception of benefits and preparedness for IFRS application.

This paper investigates the moderating effects of manager’s support on the relationship between perception of IFRS and preparedness for IFRS application. Figure 1 illustrates the proposed relationships.

The proposed research model (Source: Authors’ suggestion)

Methodology

Research context

According to the IFRS Foundation53, 166 countries and regions have implemented IFRS for listed firms within their boundaries. As of December 31st, 2020, Vietnam had signed fifteen free trade agreements with other countries and was compelled to adopt IFRS in line with prevailing global trends. The government had approved a proposal for financial reporting standards in Vietnam on March 16th, 2020. This proposal aimed to establish plans, strategies, publications, and support mechanisms for IFRS adoption among specific groups. By 2025, enterprises in Vietnam will be required to apply IFRS, but the majority of these enterprises face resource constraints. Consequently, implementing of IFRS is expected to pose more significant challenges for these enterprises. These issues can be attributed to two major reasons. Firstly, employees cannot prepare financial statements according to IFRS standards. Secondly, the infrastructure of these enterprises is not conducive to IFRS standards due to its outdated nature. Given the imminent implementation of the IFRS plan in Vietnam, it becomes essential to explore whether enterprises are willing to apply IFRS. Therefore, investigating the preparedness for IFRS application in Vietnam becomes necessary.

Measures

For the translation of the questionnaire from English to Vietnamese, the author employed the reverse translation method54. Initially, a translator expert translated the original questionnaire into Vietnamese. Subsequently, a bilingual expert, who was unaware of the study's objectives and did not have access to the original questionnaire, translated the Vietnamese version back into English. Furthermore, the author conducted a qualitative study to refine and introduce items that are pertinent to the research context. This qualitative research involved seven experts who hold senior management positions at large enterprises, each with over 20 years of experience in strategizing and operating within the business sector.

Preparedness for IFRS application. According to Guerreiro, Rodrigues and Craig 55, preparedness for IFRS application is defined as follows: “Preparedness to adopt IFRS is also linked to the procedures that companies develop to gain expertise in IFRS. A company that has assessed the impact of IFRS on its financial accounting information processing system and the training needs of its employees will be better prepared to adopt IFRS than a company that has only evaluated the changes that may occur in its financial statements. Similarly, a company that has initiated the conversion to IFRS by providing training to employees and making the necessary changes to its financial accounting information processing system will be better prepared to apply IFRS than a company that only provides employee training”. Three items were used to measure preparedness for IFRS application in Guerreiro, Rodrigues and Craig 55. Sample items include “Preparing the financial reporting system”, “Training accounting and finance department staff”, and “Preparing addition accounting information”.

Perception of challenges. Perceived challenges of IFRS refer to the obstacles, difficulties, and complexities that organizations anticipate or believe they may encounter while adopting and implementing IFRS in their financial reporting and accounting practices17. Three items were used to measure rhe perceived challenges of IFRS in Phan, Joshi and Mascitelli 17. Sample items include: “Insufficient guidance”, “Educate financial staff”, and “Limited coverage in accounting curriculum”.

Perception of disadvantages. Perceived disadvantages of IFRS refer to the potential drawbacks, challenges, or negative consequences that organizations anticipate or believe may result from adopting and applying of IFRS in their financial reporting and accounting practices 17. Three items were used to measure the perceived disadvantages of IFRS in Phan, Joshi and Mascitelli 17. Additionally, the author included two items based on qualitative research. Therefore, the scale of the perceived disadvantages of IFRS includes five items. Sample items include: “Cost outweigh benefits of IFRS adoption”, “IFRS is in foreign language thus hard to understand”, “IFRS reporting is time consuming”, “High cost of acquiring technology necessary for preparing IFRS”, and “Unwilingness of staff to acquire IFRS training”.

Perception of benefits. Perceived benefits of IFRS refer to the positive outcomes, advantages, and improvements that organizations anticipate or believe will result from adopting and applying IFRS in their financial reporting and accounting practices 17. Three items were used to measure the perceived benefits of IFRS in Phan, Joshi and Mascitelli 17. Additionally, the author included a new item based on qualitative research. Therefore, the scale of the perceived benefits of IFRS includes four items. Sample items include: “IFRS-complied report is reliable”, “IFRS-complied report is comparable”, “IFRS-complied report increases investor’s confidence”, and “Increased firm value”.

Manager’s support. Managerial support refers to the active endorsement, assistance, and facilitation managers provide to achieve specific goals, projects, or initiatives56. According to Parker and Price 56, the author developed the scale of managerial support based on qualitative research. This scale includes four items, and sample items include “Positive attitude towards IFRS application”, “Supporting human resources for IFRS application”, “Supporting financial resources for IFRS application”, and “Support for changes proposed by the government related to IFRS application”.

Sample and Procedure

Data collection for this study was conducted using offline questionnaires between November 2021 and March 2022. A language expert translated a questionnaire survey into Vietnamese and administered it to managers working at large companies in Southern Vietnam. The author visited these firms and explained the purpose of the study to the managers, who then granted permission to conduct the survey. A total of 325 questionnaires were collected, of which 238 were deemed suitable for use in this study.

The study summarizes the characteristics of the respondents based on the collected data. The distribution of respondents by the number of employees is as follows: 10.5% have below 200 workers, 8% have 200-300 workers, and 81.5% have above 300 workers. The respondents’ positions are as follows: 1.7% are general directors/directors, 23.9% are chief financial officers, and 74.4% are chief accountants (see details in Table 1).

Summary statistics

|

Characteristics |

N |

% |

|

Number of employees | ||

|

Below 200 |

25 |

10.5 |

|

200 - 300 |

19 |

8 |

|

Above 300 |

194 |

81.5 |

|

Postion | ||

|

General Director/Director |

4 |

1.7 |

|

Chief Financial Officer |

57 |

23.9 |

|

Chief Accountant |

177 |

74.4 |

Results

Measurement model

The general methodology may introduce potential bias due to data collection procedures and including respondents from different companies. To address this concern, a Harman’s one-factor experiment was conducted. The results of the Harman test revealed that the first factor accounted for only 29.582% of the variance, which is below the 50% threshold. This suggests that the study does not exhibit bias in the response data 57. Additionally, the measurement model assesses the composite reliability and validity of the structural model, demonstrating that rigorous methodologies were employed to analyze the expected model 58.

Results of the measurement model

|

Constructs |

Item |

VIF |

Factor loading |

Cronbach’s Alpha |

CR |

AVE |

|

Preparedness for IFRS application |

PREP1 |

2.091 |

0.883 |

0.876 |

0.923 |

0.801 |

|

PREP2 |

2.736 |

0.911 | ||||

|

PREP3 |

2.536 |

0.891 | ||||

|

Perception of challenges |

PERC1 |

1.946 |

0.887 |

0.784 |

0.816 |

0.696 |

|

PERC2 |

1.604 |

0.851 | ||||

|

PERC3 |

1.569 |

0.760 | ||||

|

Perception of disadvantages |

PERD1 |

3.407 |

0.858 |

0.897 |

0.922 |

0.702 |

|

PERD2 |

3.373 |

0.876 | ||||

|

PERD3 |

3.264 |

0.801 | ||||

|

PERD4 |

2.534 |

0.834 | ||||

|

PERD5 |

3.056 |

0.819 | ||||

|

Perception of benefits |

PERB1 |

3.479 |

0.911 |

0.890 |

0.922 |

0.749 |

|

PERB2 |

2.392 |

0.791 | ||||

|

PERB3 |

1.940 |

0.846 | ||||

|

PERB4 |

3.666 |

0.908 | ||||

|

Manager’s support |

MANS1 |

2.476 |

0.844 |

0.884 |

0.920 |

0.742 |

|

MANS2 |

3.009 |

0.878 | ||||

|

MANS3 |

1.994 |

0.819 | ||||

|

MANS4 |

3.740 |

0.902 |

The author analyzed the convergent validity using measures such as Cronbach's alpha, composite reliability, and average variance extracted (Table 2). After testing, it was found that the factor loading for all variables is higher than 0.7, and the values for composite reliability, Cronbach's alpha, and average variance extracted for all variables are higher than 0.7, 0.7, and 0.5, respectively. Moreover, the variance inflation factor (VIF) for all variables is lower than 4, suggesting that the model does not exhibit multicollinearity59.

Fornell-Lacker Criterion and Heterotrait-Monotrait Ratio (HTMT)

|

Fornell-Lacker Criterion | |||||

|

MANS |

PERB |

PERC |

PERD |

PERP | |

|

MANS |

0.861 | ||||

|

PERB |

0.155 |

0.866 | |||

|

PERC |

-0.136 |

0.032 |

0.835 | ||

|

PERD |

-0.149 |

-0.391 |

-0.156 |

0.835 | |

|

PERP |

0.538 |

0.337 |

-0.322 |

-0.265 |

0.895 |

|

Heterotrait-Monotrait Ratio (HTMT) | |||||

|

MANS |

PERB |

PERC |

PERD |

PERP | |

|

MANS |

- | ||||

|

PERB |

0.172 | ||||

|

PERC |

0.160 |

0.095 | |||

|

PERD |

0.140 |

0.395 |

0.195 | ||

|

PERP |

0.608 |

0.367 |

0.379 |

0.283 |

- |

The validity of discrimination is examined based on the Fornell and Larcker60 indicator after analyzing convergent validity. The results of the Fornell-Larcker criterion show that the discrimination values are higher than other indicators along the diagonal line (Table 3). Therefore, the discrimination values meet the required criteria59. Table 3 presents that the coefficients in the Heterotrait-Monotrait test are all below 0.9, indicating that the scales meet the criteria for discriminant validity61.

Structural model

The author employed partial least squares–structural equation modeling (PLS-SEM) to estimate the paths in the structural model. Table 4 and Figure 2 present the results of the structural model.

Stuctural Model Assessment (Source: Authors’ suggestion)

Results of the structural model

|

Hypothesis |

Relationship |

Original Sample |

Sample Mean |

Standard Deviation |

T statistics |

p value |

Decision |

|

H1a |

PERC -> PREP |

-0.388 |

-0.388 |

0.056 |

6.869 |

0.000 |

Accepted |

|

H1b |

PERD -> PREP |

-0.240 |

-0.251 |

0.053 |

4.516 |

0.000 |

Accepted |

|

H1c |

PERB -> PREP |

0.232 |

0.230 |

0.056 |

4.130 |

0.000 |

Accepted |

|

H2 |

MANS -> PREP |

0.454 |

0.454 |

0.058 |

7.836 |

0.000 |

Accepted |

|

H3a |

PERC*MANS -> PREP |

-0.206 |

-0.200 |

0.064 |

3.219 |

0.001 |

Accepted |

|

H3b |

PERD*MANS -> PREP |

0.005 |

-0.001 |

0.061 |

0.087 |

0.930 |

Rejected |

|

H3c |

PERB*MANS -> PREP |

-0.067 |

-0.067 |

0.064 |

1.048 |

0.295 |

Rejected |

According to Table 4, the coefficients of the perception of benefits variable, and manager’s support variable are positive and significant at the 1% level. In contrast, the coefficients of the perception of challenges variable and the perception of disadvantages variable are negative and significant at the 1% level. Similarly, the coefficient of the interaction variable between the perception of challenges and the manager’s support is negative and significant at the 1% level. When considering other variables, the coefficients of interaction variables between manager’s support and perception of disadvantages and perception of benefits are not significant at the 10% level (refer to Table 4).

Discussion

This study aims to analyze the moderating effect of manager’s support on the relationship between the perception of IFRS and oreparedness of IFRS application in the proposed model. The findings reveal some interesting results that contribute to existing studies on preparedness for IFRS application.

Table 4 reveals that the perception of challenges coefficients are significantly negative at the 1% level, indicating that the perception of challenges has a negative effect on the preparedness for IFRS application and supporting hypothesis H1a. This result is in line with those of Phan, Joshi and Mascitelli 17, who found that the perception of challenges can decrease the level of preparedness for IFRS application. The findings of this study can be explained due to several reasons. First, perceiving challenges of IFRS can impact organizational culture and processes 62. Managing resistance to IFRS adoption is crucial for preparedness. Second, organizations perceiving risks in IFRS adoption, like financial misstatements or compliance issues, must invest time in evaluating and mitigating them, impacting preparedness 1. Third, perceiving challenges may involve technical infrastructure concerns for IFRS reporting, necessitating system and software upgrades, planning, and resources 63. Fourth, organizations perceiving legal and regulatory challenges in new or unfamiliar IFRS jurisdictions must navigate these issues, affecting their preparedness64. Finally, perceiving IFRS as a global standard can affect preparedness, especially for organizations targeting international markets or IFRS-favored investors 65.

The findings also confirmed a negative association between the perception of disadvantages and the preparedness for IFRS application at a 1% significance level (refer to Table 4). Therefore, the author had sufficient evidence to accept H1b, suggesting a negative association between the perceived disadvantages and the preparedness for IFRS application. This result is similar to the viewpoint of Hu 29, who argued that the perception of disadvantages is negatively associated with the preparedness for IFRS application. Moreover, perceiving a lack of expertise in their internal accounting and finance teams for IFRS implementation can be concerning66. It may necessitate staff hiring or training, potentially delaying preparedness. Similarly, perceiving IFRS adoption as a potential disruption to daily operations can be a deterrent, as organizations worry about its impact on processes and productivity67. Uncertainty about investor, creditor, and stakeholder reactions to IFRS adoption can impact preparedness, especially if the market is expected to respond negatively 68. Concerns about the transition timeline to IFRS may disrupt financial reporting and operations 69.

A positive relationship exists between the perception of benefits and the preparedness for IFRS application at a 1% significance level (refer to Table 4). Therefore, the author had sufficient evidence to accept H1c, suggesting a positive association between the perception of benefits and the preparedness for IFRS application. This finding is consistent with the results of Phan, Joshi and Mascitelli 17. The findings of this study can be explained by several ways. First, the belief that IFRS boosts investor confidence through its transparency and consistency can drive preparedness, especially for organizations seeking external financing 70. Second, perceiving IFRS as a simplifier of financial reporting and compliance complexity can motivate preparedness, potentially leading to cost savings71. Third, organizations planning M&A activities may see IFRS adoption as an advantage, facilitating smoother transactions and integration with IFRS-compliant companies72. Fourth, the expectation of higher-quality financial information with IFRS can motivate preparedness and enhance decision-making 73. Finally, perceiving IFRS as reducing information asymmetry between management and external stakeholders can drive preparedness, potentially leading to more efficient capital markets 74.

At a 10% significance level (refer to Table 4), a positive impact of the manager’s support on the preparedness for IFRS application is observed. Therefore, the author had sufficient evidence to accept H2, suggesting a positive association between the manager’s support and the preparedness for IFRS application.

The moderating effect of the manager’s support on the relationship between the perception of challenges and the preparedness for IFRS application (Source: Authors’ calculations).

The coefficient of the interaction variable between the perception of challenges and the manager’s support is negative and significant at the 1% level (refer to Table 4). To examine the stability of the hypothesis, the author employed a graph that distinguishes between high and low manager support groups through the average value of the manager’s support variable. The results in Figure 3 reveal that there is a difference in the relationship between the perceived challenges and the preparedness for IFRS application depending on the level of the manager’s support. Therefore, the author had sufficient evidence to accept hypothesis H3a, indicating that the manager’s support modifies the relationship between the perception of challenges and the preparedness for IFRS application. Specifically, the negative relationship is weaker when the manager’s support is high.

The coefficients for perceptions of disadvantages and benefits are not statistically significant at the 10% level, indicating that managerial support cannot moderate the impact of these perceptions on preparedness for IFRS application. Thus, hypotheses H3b and H3c are rejected (refer to Table 4). The study results can be explained by the fact that Vietnam is still in the preparation stage for IFRS application, so it is possible that business managers have not yet focused significantly on the benefits and disadvantages of implementing and applying IFRS. Consequently, this study does not examine the moderating impact of managerial support on the relationship between perceptions of disadvantages, perceptions of benefits, and preparedness for IFRS application.

Conclusions

This study examines how the manager’s support moderates the relationship between the perception of IFRS and the preparedness for IFRS application. Based on data from 238 respondents, the findings of this study found that the perception of benefits and manager’s support have a positive impact on the level of preparedness for IFRS application. In contrast, the perception of challenges and the perception of disadvantages are negatively associated with the level of preparedness for IFRS application. Additionally, the manager’s support can moderate the negative relationship between the perceived challenges and the preparedness for IFRS application.

Theoretical contributions

The findings of this study are some theoretical contributions follow as:

Firstly, this research contributes to applying agency theory in the context of IFRS adoption. The finding provides insights into how the perception of IFRS can affect the agency relationship between managers and shareholders and how managerial support can moderate this relationship. This application of agency theory can help expand our understanding of how governance mechanisms operate in the context of accounting and financial reporting standards.

Secondly, by exploring how managerial support influences an organization's preparedness for IFRS application, this research contributes to the understanding of factors that impact preparedness. It sheds light on the role of leadership and management in shaping an organization's readiness for significant accounting and reporting changes.

Thirdly, the findings can have practical implications for organizations considering or undergoing IFRS adoption. Understanding the moderating effect of managerial support can inform strategic decisions related to leadership involvement and support in the adoption process. This can help organizations better navigate the challenges and opportunities associated with IFRS adoption.

Finally, this research can also contribute to change management theory by examining the role of managerial support as a critical factor in mitigating resistance to change within an organization. It can offer insights into how leadership can facilitate a smoother transition to new accounting standards.

Managerial implications

The findings of the study show some managerial implications for improving the moderating effect of manager’s support on the relationship between the perception of IFRS and the preparedness for IFRS application follow as:

Firstly, managers and leaders should actively participate in adopting IFRS. Their support and commitment to the transition are crucial for overcoming potential challenges and ensuring that the organization is prepared for the change.

Secondly, understanding managerial support's role support in mitigating the impact of perceived challenges or disadvantages can help organizations align the interests of management and shareholders. Managers can play a key role in ensuring that the transition to IFRS is in organization's and its stakeholders' best interest.

Thirdly, organizations should develop effective change management strategies that consider the importance of managerial support. This includes strategies for communicating the benefits of IFRS adoption, addressing concerns, and actively involving managers in the planning and executing of the transition.

Fourthly, managers should have the knowledge and skills required for IFRS adoption. Providing training and development opportunities for management and finance teams can enhance their ability to support the transition effectively.

Finally, organizations should establish mechanisms to monitor and evaluate the level of managerial support throughout the IFRS adoption process. This can help identify areas where additional support or resources may be needed and ensure that managerial commitment remains consistent.

Limitations and future directions

While this study offers valuable insights, it is important to acknowledge certain limitations that provide avenues for future research. Firstly, the data collection for this study focused on large firms located in Southern Vietnam. Future studies could broaden their scope by gathering data from diverse regions within Vietnam to explore potential regional variations. Secondly, this research was conducted in an emerging economy, Vietnam. Subsequent studies could extend their investigations to other countries to assess potential cross-cultural similarities and differences in preparedness for IFRS application. Finally, future research endeavors could include additional variables, such as firm characteristics, industry type, and access to external expertise, among others, to gain a more comprehensive understanding of the factors influencing preparedness for IFRS application.

NOTE

The data will be available on request.

FUNDING

No funding was received.

ABBREVIATIONS

PREP: Preparedness for IFRS application

PERC: Perception of challenges

PERD: Perception of disadvantages

PERB: Perception of benefits

MANS: Manager’s support

VIF: Variance inflation factor.

CR: Composite reliability.

AVE: Average variance extracted.

CONFLICT OF INTEREST

The author declare that they have no conflicts of interest.

AUTHORS’ CONTRIBUTION

The author is a major contributor to this study.

Appendix

Measurement items

|

Research construct |

Items |

Source |

|

Perception of benefits |

Businesses applying IFRS help increase investment attraction. |

Phan, Joshi and Mascitelli |

|

Businesses applying IFRS help increase business value. | ||

|

Financial statements based on IFRS are comparable. | ||

|

Financial reporting based on IFRS increases investor confidence. | ||

|

Perception of disadvantages |

Employees may not desire IFRS training. |

Phan, Joshi and Mascitelli |

|

Financial reporting based on IFRS can be time-consuming. | ||

|

Some businesses may incur costs that outweigh the benefits of applying IFRS. | ||

|

Since IFRS is in a foreign language, it can be challenging to understand. | ||

|

High cost of acquiring technology necessary for preparing IFRS | ||

|

Perception of challenges |

Incomplete guidance on applying IFRS. |

Phan, Joshi and Mascitelli |

|

The retraining of staff and managers in the finance and accounting department. | ||

|

Accounting curricula at universities mention very little about IFRS. | ||

|

Manager’s support |

Managers have a positive attitude towards applying IFRS. |

Parker and Price |

|

Managers support human resources in applying IFRS. | ||

|

Managers support financial resources in applying IFRS. | ||

|

Managers support changes proposed by the government related to IFRS application. | ||

|

Preparedness for IFRS application |

Enterprises are ready to prepare training plans for accounting department staff to meet IFRS. |

Guerreiro, Rodrigues and Craig |

|

Enterprises are ready to prepare more information about implementation steps and technology systems to meet IFRS. | ||

|

Enterprises are ready to prepare financial plans to meet IFRS. |